Amazon Prime Day Deals 2024

General Deals

- Audible Premium Plus: 3 Months Free

- Amazon Music Unlimited: 5 Months Free

- Amazon Kindle Unlimited: 3 Free Months

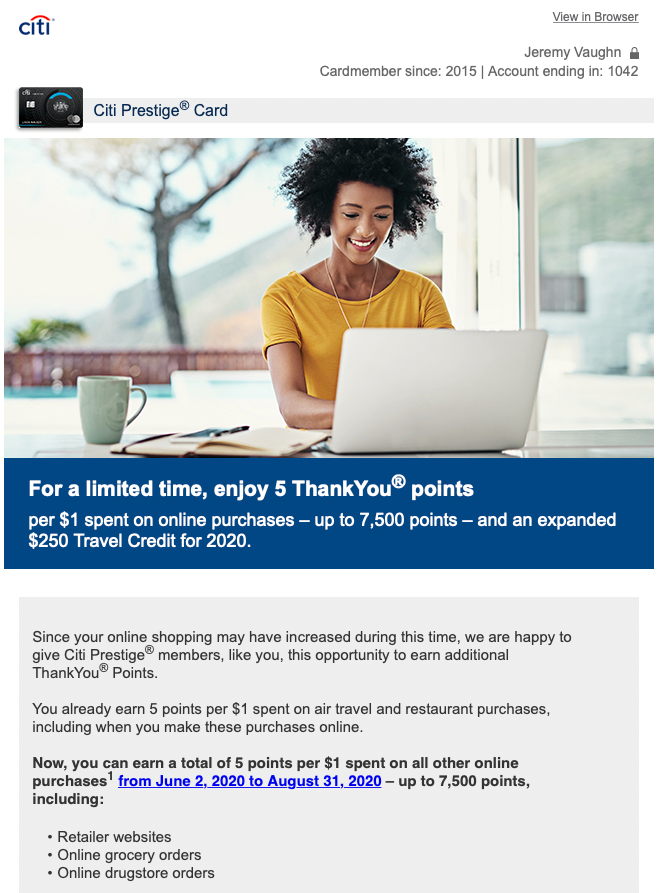

- Chase Amazon Prime Visa $200 Signup Bonus With No Spend Required through 7/26

- Amazon Prime: Get $20 Off $30 Amazon credit when you back up photos with Amazon Photos

- Amazon Fresh Stores: $15 Off $75 through 7/15

- Amazon Grocery Unlimited Delivery: 90-day free trial

- Prime members save 15% when buying $50 of select items

- $15 Credit With $50 Spend On Household Essentials

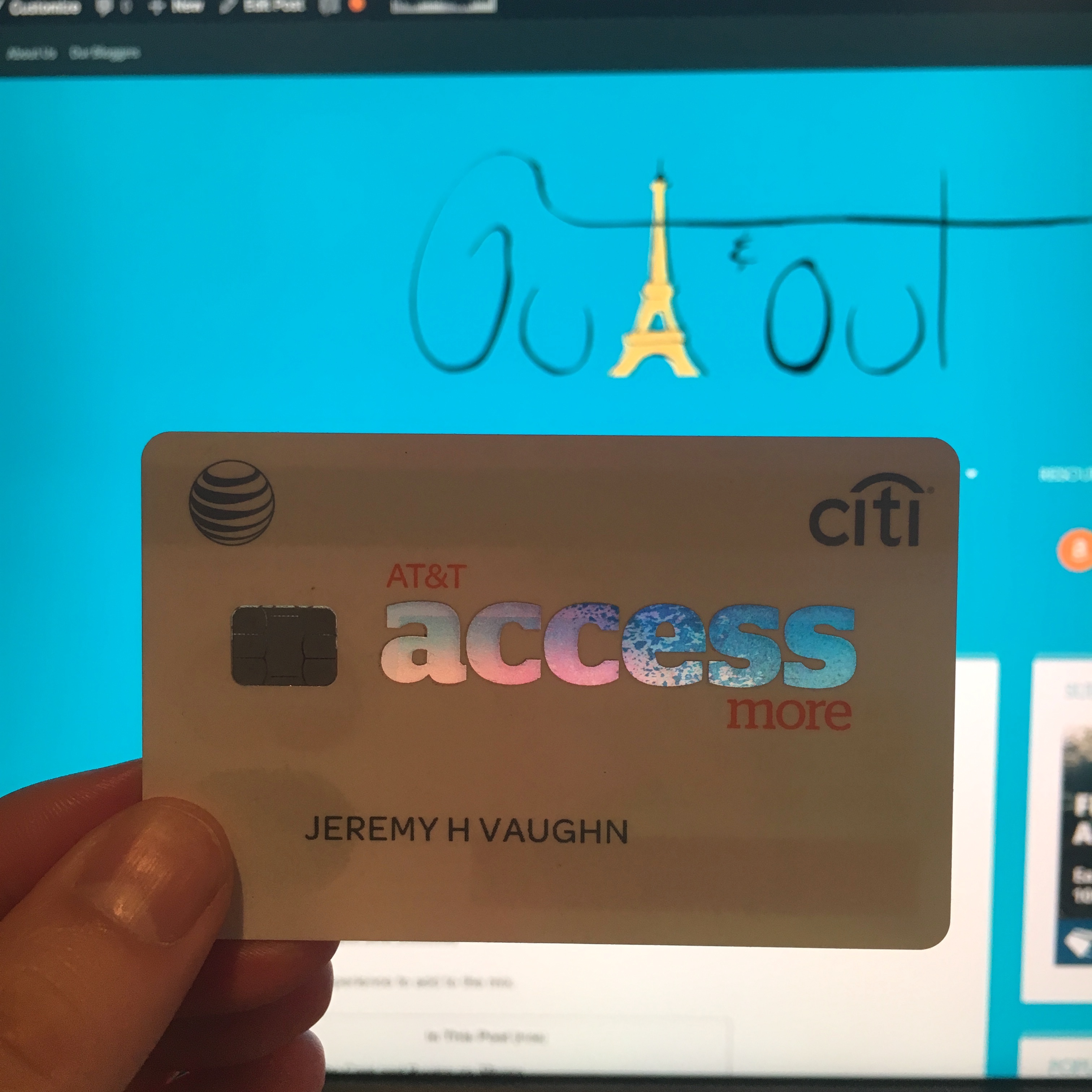

- Amazon Prime Visa Card: 10% Back On Select Items

$200 smackaroos and 5% back (note: it’s a Chase card)