Dang, the last time I did a full credit card inventory was three years ago. Can you believe?

Back then, I had 29 cards. These days I have 23, and currently have my eye on three more (ironically, all cards I’ve had before: Chase Sapphire Preferred, Citi Premier, and US Bank Altitude Reserve).

Of the 29 I had, some I closed, some were discontinued, and others were canceled for me. And I still have a lot of them today. Let’s hop to it!

Recent mainstays

I set up each section with:

Name of card – annual fee amount – # of years I’ve had it – keep or cancel

Amex

I used to be jamming with several Amex cards. But these daze, I’m down to just three. I just can’t with the airline and other goofy credits they used as justification to jack up their annual fees.

I am semi-interested in the Amex Gold card because of its strong category bonuses, but with that $250 annual fee? No thanks.

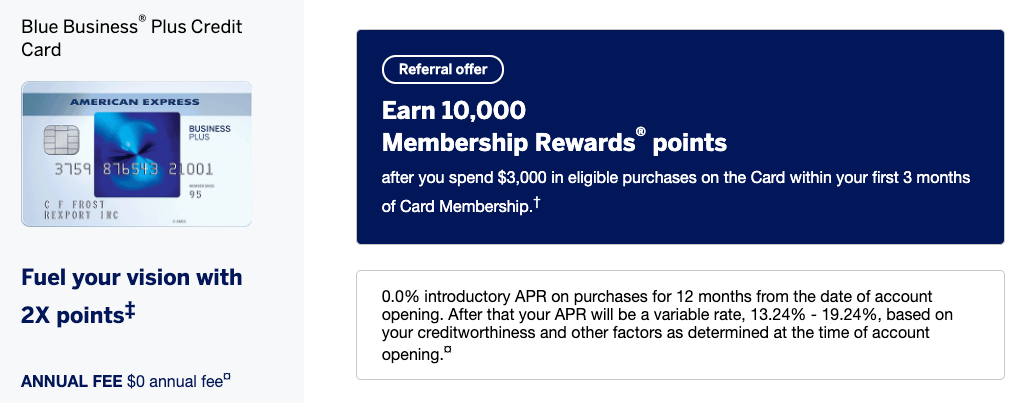

1. Blue Business Plus – $0 – 4 years – Keep

No annual fee, 2X Amex Membership Rewards points on up to $50,000 in purchases per calendar year, AND the ability to transfer points to travel partners? Whaaat? This card is an absolute forever keeper.

Plus, thanks to Amex Offers, I actually make money from keeping this card.

What you waiting for?

There’s no official welcome offer, but you can use my referral link to earn 10,000 Amex Membership Rewards points after spending $3,000 on purchases within your first three months. This card doesn’t show up on your personal credit report because it’s a small business card. If you’ve never had it, I highly recommend it.

2. Hilton Aspire – $450 – 4 years – Keep

- Link: Hilton Aspire

Amex has kept this card stacked with benefits and has never raised the $450 annual fee since it came out, including:

- 14X Hilton points on purchases at Hilton

- 7X Hilton points on flights booked directly with airlines on on Amex Travel

- 7X Hilton points at US restaurants

- 3X Hilton points for all other purchases

- Up to $250 in Hilton resort credits per year

- A free weekend reward night upon renewal each year

- Up to $250 in annual airline fee credits

- Diamond elite status, which gets you upgrades, free breakfast, bonus points at Hilton, and access to club lounges on every stay

- Priority Pass Select membership

- Terms Apply

If you like Hilton hotels, this card is an absolute keeper. The annual fee easily pays for itself.

Outside the Hilton Austin a year ago

I prefer Hilton hotels, and will keep this card for as long as the benefits remain this generous.

3. Hilton no annual fee – $0 – 5 years – Keep

- Link: Amex Hilton card

I downgraded an old Hilton Surpass to this no annual fee card. It’s basic, but there’s no annual fee so I’ll keep it.

Barclays

4. AAdvantage Aviator no annual fee – $0 – 3 years – Keep

I downgraded my AAdvantage Aviator Red card (which has a $95 annual fee) to this one because there’s no annual fee. Barclays like to keep relationships with customers, so it’s helpful if I ever want another of their cards in the future.

Chase

I currently have eight Chase cards – the most of any bank!

5. Ink Business Preferred – $95 – 2 years – Cancel

I mostly got this card for the stellar welcome offer, but find myself not using it much. Can go in the bin next time the fee is due.

6. Ink Plus – $95 – 6 years – Keep

This card is no longer available to new applicants and offers 5X Chase Ultimate Rewards points on office supply purchases, cable, internet, phone bills, and oddly enough – streaming services.

It’s a bit niche, but 5X for my streaming stuff is nice

I keep it for the bonus categories and also to preserver the ability to transfer my Chase Ultimate Rewards points to travel partners – mostly Hyatt. The airline partners are all a bit crappy tbh.

7. British Airways no annual fee – $0 – 3 years – Likely cancel

Yes, there’s a no fee version of the British Airways card. I was surprised too. When a representative offered it to me, I said sure.

What will mostly likely end up happening is I’ll offer to close this card when I get ready to open a new Chase Sapphire Preferred card, as I don’t think Chase would let me have nine cards. So I’ll keep this one as leverage for that time.

8. Freedom – $0 – 18 years – Keep

My oldest card. I got it when I was 18. And I’ll be 36 next month. Crazy!

This card keeps my accounts aged nicely and my credit score high.

My Chase Freedom helps my AAoA pretty high

Plus, I use the card often thanks to rotating quarterly bonus categories. Which reminds me, I need to activate the bonus for this quarter.

9. Freedom Unlimited – $0 – 8 years – Keep

This was my old Sapphire Preferred, but I downgraded it to this. I use it at Costco and that’s about it – and only because Costco only accepts Visa. It doesn’t get much love otherwise. :/

10. Hyatt (old version) – $75 – 7 years – Keep

I’ve always found a creative use for the Hyatt free night, except for maybe this year. Even if I can’t redeem it because of coronavirus, I’ll hang onto it because:

- Coronavirus won’t last forever (right?!)

- It’s a slightly older card, so it helps boost my overall credit

I do love Hyatt though, and hope to be back in their hotels soon.

11. IHG Select (old version) – $49 – 5 years – Keep

Same deal at the Hyatt card above. I like the annual free night, but don’t encounter many IHG hotels otherwise.

My IHG stay earlier this month was my first and likely last for a while

12. United Explorer – $95 – 4 years – Keep

I was keeping this card to:

- Get more United award space

- Use the two lounge passes per year

- Keep my United miles alive

Now that I’m not traveling and United miles no longer expire, keeping this card is a bit… dubious.

But like the hotel cards, I’m mostly keeping it out of hope at this point. It would be second on the chopping block after the British Airways card if I do end up canceling. I just paid the annual fee right when coronavirus started bearing down, so I’ll give it until next year to see what happens.

Citi

Now Citi… we love. I use their cards more than any others and have six in total. Their bonus categories, earning structures, and the way the card benefits stack across cards works great for my spending patterns.

Plus, there’s a huge overlap in airline transfer partners with both Chase and Amex. I love my ThankYou points!

13. CitiBusiness AAdvantage Platinum Select – $95 – 3 years? – Cancel

I was keeping this card for the American Airlines benefits. Living in Dallas and having no desire to earn any type of airline elite status, I found myself on American Airlines more often than not.

The enhanced boarding and free checked bag was worthwhile, but I’ll likely cancel when the fee comes due and just get another one later because they’re easy enough to get. Probably from Barclays so I can keep my Citi slots open.

14. AAdvantage MileUp – $0 – 8 years – Keep

Free to have, downgraded from an old AA card. Never use it though. Maybe I should after my recent incident. 😬

15. AT&T Access More – $95 – 5 years – Keep

Love it, use it often, always get retention offers. And it’s no longer available to new applicants, so I’ll keep it as long as I can.

I’ve always gotten the 10,000 annual bonus points, so it more than covers the annual fee.

16. Double Cash – $0 – 3 years – Keep

Now that the rewards on this card transfer to ThankYou points at a 1:1 ratio, I use it all the diddy dang time. It’s my catch-all, “everything else” card. 2X Citi ThankYou points per $1 spent with no cap or bonus categories to remember. Swipe swipe swipe.

Love having this card to earn unlimited 2X Citi ThankYou points

This one has truly ascended to the top of the pile. Will keep forever in its current form.

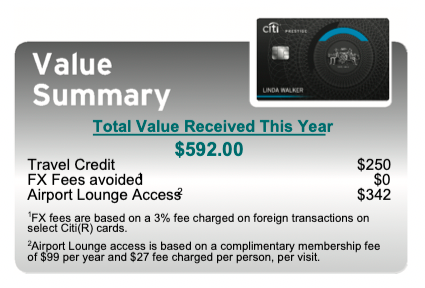

17. Prestige – $495 – 5 years – Keep???

I’m on the fence with this one because I can’t use the travel benefits and I’m not dining out often enough to use the 5X dining multiplier. My annual fee is due again in November, so we’ll see.

In normal times, this card is worth its salt

I might get the Citi Premier card to replace it.

This one’s on thin ice. Nearly constant changes and now a card I can’t really use isn’t boding well though I used to adore it. Kinda sad – I get attached to my cards lol.

18. Rewards+ – $0 – 5 years – Keep

Free to keep and the 10% points rebate stacks with any other ThankYou card. Easiest keep I ever did see.

The rest

19. Alaska Visa – $75 – 2 years – Cancel

This is actually my newest card of the entire bunch! But I only got it for the welcome offer. I don’t see myself flying on Alaska Airlines any time soon, so I’ll cancel and get another one down the road.

Only hitch is that it’s also the only card where I’m carrying a balance because of a 0% APR offer through September 2021. So once that’s paid off (and it’s heavily on my radar), I’ll close it.

20. Fidelity Visa – $0 – 7 years – Keep

Always nice to have another 2% option, but it’s no contest – I’ll use my Amex Blue Business Plus or Citi Double Cash over this one any day. They have promos sometimes, so it passes muster… barely

21. USAA Signature Visa – $0 – 2 years – Keep

I bought my rowing machine with this card’s 0% APR offer and now it’s one of my prized possessions

I got this card when I did a stint in Austin because it had a 0% APR offer and I was stretched to the max while trying to move. I’m still dealing with that situation (see #19 above). But I have this card now, and it’s my second newest so might as well keep it for a while.

Also, back when I got it, I was locked out of most other card options (5/24, Amex once per lifetime rules, Citi’s weird rules, etc.). It’s not a card I’d ever use for everyday spending.

22 and 23. Two of the same card from a bank I’m forbidden to mention – Keep

They both have a $0 annual fee, so I’m keeping them for perpetuity. The powers that be say I “may not mention [redacted], their intellectual property, card names, card images, or points program names on any page that links to CardRatings” (my credit card affiliate network) on tablets made of stone. So I never mention them.

But this is a credit card inventory, so I don’t really know how to include them in the list without skirting the issue. So yeah. Fine cards I can’t mention. Keeping them.

Initial thoughts

Just surveying the card inventory here, I:

- Don’t really mess with Amex any more, which is surprising

- Have lots of Chase cards I can’t/don’t use

- Am super into Citi ThankYou over the last few years

- Have really trimmed my card portfolio to just a couple of banks (14 out of 23 cards are with Chase or Citi)

Credit card inventory bottom line

- Link: Apply for Card Offers

Of my 23 current cards:

- 19 are keepers

- 4 are on the chopping block

Of the 19 I plan to keep, I’ll pay $1,354 in annual fees. I’ll get back or have already gotten back $250 from Hilton Aspire and $250 from Citi Prestige. That brings my net cost down to $854. And across all these cards I’ll also get:

- A free night at a IHG hotel (Chase IHG)

- A free night at a Hyatt Category 4 hotel (Chase Hyatt)

- 10,000 Citi ThankYou points (Citi AT&T Access More)

- Priority Pass Select membership for lounge access (Amex Hilton Aspire and Citi Prestige)

- A free weekend night at nearly any Hilton hotel (Amex Hilton Aspire)

- 25% more miles through MileagePlus X (Chase United Explorer)

- More United award space and two United Club lounge passes worth $50 each (Chase United Explorer)

- Many, many Amex Offers (Amex cards)

Plus bonus points on nearly every single dollar I spend. Is all that worth $854?

When I add it all up, yes, it’s all worth much more than that – maybe a few times over. But it’s hard to say right now.

This is a strange time to be a travel blogger who can’t travel. I’d love to use all my cards and their benefits, but have to press the pause button on this analysis and hope for the best outcome.

I’m torn about opening new cards to earn welcome offers right now as well. On one hand, it’s nice to have a stockpile. On the other, why earn if you can’t burn?

How does your current collection compare? Are you applying for new offers or holding off until “after” the pandemic? Are you switching up cards to suit your new spending patterns like I am?

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Hey! Just read your informative post on credit cards. Which cards do you actually use frequently?

Right now I’m using my Citi Prestige for dining and Citi Double Cash for most everything else. I’m using the Amex Hilton Aspire through 7/31 to earn 12X Hilton points on groceries, then switching to Chase Freedom until the end of Q3 to take advantage of the 5X categories going on until then.

And honestly… that’s about it. Although I am thinking of getting Citi Premier for its new 3X bonus categories on flights, dining, gas, and groceries – seems like it could be perfect for current pandemic spending. And then the US Bank Altitude reserve for its sign-up bonus and 3X on mobile payments (including at Costco, since it’s a Visa).

I usually have more variety with my cards, but for now I’m getting by with Citi Prestige and Double Cash.

Perhaps the most obvious thing I see is that Prestige talks about the airline lounge access, but due to Covid-19, that’s not terribly useful right now. I held on to my Prestige until they upped the AF, and I was barely seeing enough benefit to offset the steep $495 AF. For a card with that high of an AF, it should offer travel benefits, especially if Citi is whittling down what qualifies as travel, or how to use other card benefits.

It’s definitely on my chopping block this December if things don’t turn around in the next few months. Might just go all-in with the Citi Premier though I will really REALLY miss the 5X on dining. But I agree, without the lounge access I’m not sure if it’s worth keeping.

Since you have Citi Double Cash and Amex Blue Business Plus, why not convert the Freedom Unlimited to a regular Freedom card? I’m guessing you hardly use the Freedom Unlimited and it’s nice to have the extra 5x space available for good categories.

I already have both (a Freedom and a Freedom Unlimited). They’re both free to keep, so it makes sense. Haven’t been overly thrilled about their 5X categories lately. But using them when I can. The Amazon/Whole Foods this quarter is a pretty good one. Is it just me or did they used to be a lot better and more competitive?

Nice to see groceries if only Amazon/WFM. You may want to rethink your strategy with the new Flex cards. I personally would like the $3k limit instead of $1.5k limit per quarter, but to each his/her own. I had a CFU before (for a SUB) and converted it to CF after my year was up. Don’t regret in the least as I NEVER used the CFU outside the SUB.