How much do you have to spend each year for a Chase Sapphire annual fee to be worth it? The answer depends on:

- Whether you spend in the bonus categories often

- How much you value Chase Ultimate Rewards points

It depends on your spending habits, but let’s take a looky-loo

I’ll break down spending in 3 scenarios:

- Half bonus/half non-bonus spending with points worth their base rate for each card

- Half bonus/half non-bonus spending with points worth 2 cents each

- All bonus spending with points worth 2 cents each

Boom!

1. Chase Sapphire Preferred

- Link: Chase Sapphire Preferred – Compare this card

- Link: The Top Card for Beginners? Yeah, the Chase Sapphire Preferred

| Chase Sapphire Preferred® Card | bonus_miles_full |

|---|---|

| • 5X Chase Ultimate Rewards points per $1 spent on travel booked through Chase • 3X Chase Ultimate Rewards points per $1 spent on dining |

| • $95 annual fee • $50 annual hotel credit • 10% anniversary points bonus • Free DoorDash DashPass subscription | • $4,000 on purchases in the first 3 months from account opening |

| • The best card for beginners | • Compare it here |

CSP, you’re up first.

If you’re new to collecting points & miles, the Chase Sapphire Preferred is hands down the best place to begin. It’s where I started. And when anyone asks me “What’s the BEST points card if you can only have one?” (I get this question a lot), this one is the answer.

I loved this card to start with and always think of it fondly

The points you earn are worth at least 1.25 cents each because that’s their base rate on travel booked through Chase. However, I like my points to be worth 2 cents apiece, so I save them for high-value travel awards to get the best bang for my buck. Okurr?

Half/half & 1.25 cents each

Let’s say you spend roughly half on travel or dining, and the other half on everyday spending. And you use the points to book travel through Chase, where they’re worth 1.25 cents each.

To recover the cost of the $95 annual fee, you’d need to earn 7,600 Chase Ultimate Rewards points. Of those, you’d need to spend:

- $1,900 on travel and dining (to earn 3,800 points @ 2X)

- $3,800 on other purchases (to earn 3,800 points @ 1X)

Per month, you’d need to spend:

- ~$158 on travel and dining

- ~$317 on other purchases

Which is totally doable if you keep this as your everyday card. Once you recover the cost of the annual fee, all the other points you earn are yours to spend however you want!

Half/half & 2 cents each

In this scenario, you’d only need to earn 4,750 Chase Ultimate Rewards points in a single year to make the card worth keeping. It breaks down to:

- ~$1,188 on travel and dining (to earn 2,375 points @ 2X) or ~$99 a month

- $2,375 on other purchases (to earn 2,375 points @ 1X) or ~$198 a month

That’s even easier. And attainable for even casual points earners.

Full 2X & 2 cents each – My personal valuation

I added this one because this is how I personally spend and view the points. With these values, the card is an exceptional no-brainer to have and keep long-term.

Again, you’d need to earn 4,750 Chase Ultimate Rewards points to make the card worth keeping.

If you eat out a lot, the CSP is easy to justify keeping

But if all your spending is for travel and dining, you’d only need to spend $2,375 a year to earn that. That’s only ~$198 a month in those categories.

I personally spend much more in those categories. Because “travel” includes things like:

- Airbnb bookings

- Toll tags

- Parking garages

- Award bookings (taxes and fees)

- And of course air travel and hotels

Remember, travel and dining are both broadly defined

The “dining” category is broad, too – and includes:

- Fine dining

- Bars (yep!)

- Fast food

- Casual restaurants (like Panera, Start, and similar)

- Coffee shops (Starbucks, Coffee Bean, and similar)

So really, the Sapphire Preferred is worth keeping for nearly anyone if you transfer your points to travel partners.

2. Chase Sapphire Reserve

- Link: Chase Sapphire Reserve – Compare this card

- Link: Why I Product Changed to the Chase Sapphire Reserve

| Chase Sapphire Reserve® | 60,000 Chase Ultimate Rewards points |

|---|---|

| • 3X Chase Ultimate Rewards points per $1 spent on travel & dining • 1X Chase Ultimate Rewards points per $1 spent on all other purchases |

| • $550 annual fee | • $4,000 on purchases in the first 3 months from account opening |

| • Why this is my favorite card for travel and dining | • Compare it here |

Think of this card as the Sapphire Preferred’s older sibling. The one who grew up and got all fancy. 💃

Are you sick of seeing this pic yet? LMGAO

You also get:

- 3X Chase Ultimate Rewards points on travel and dining purchases

- 1X Chase Ultimate Rewards point on all other purchases

- $300 annual travel credit

- Priority Pass Select membership

- $100 Global Entry credit

- And…

The list of CSR bennies

Your points are also worth a baseline of 1.5 cents each when you book travel through Chase. This, and all the other benefits, are what prompted me to ask Chase to change my Sapphire Preferred to a Sapphire Reserve card.

Plus, the travel and dining category gets a bump to 3X per $1 spent. Let’s see how much you’d need to spend to recoup a much larger annual fee. I won’t include any of the other benefits – only spending to recover the fee.

Half/half & 1.5 cents each

Again, when you spend roughly half on travel or dining, and the other half on everyday spending. And you use the points to book travel through Chase, where they’re worth 1.5 cents each.

To recover the cost of the $550 annual fee, you’d need to spend to earn 30,000 Chase Ultimate Rewards points – much more than the Preferred. Of those, you’d need to spend:

- $5,000 on travel and dining (to earn 15,000 points @ 3X)

- $15,000 on other purchases (to earn 15,000 points @ 1X)

By month, you’d need to spend:

- ~$416 on travel and dining

- $1,250 on other purchases

Assuming this is your everyday card, you’d need to spend around $1,600 per month to justify the annual fee. With the Preferred card at these levels, you’d only need to spend $475 per month. Not the best option if you’re unsure or don’t have a clear earning focus.

Half/half & 2 cents each

Here, you’d need to earn 22,500 Chase Ultimate Rewards points in a single year to make the card worth keeping. That’s:

- $3,750 on travel and dining (to earn 11,250 points @ 3X) or ~$313 a month

- $11,250 on other purchases (to earn 11,250 points @ 1X) or ~$938 a month

It’s starting to become clear that your personal valuation of the points and how much you spend per month becomes a deciding factor of which card is best for you.

This scenario could be feasible for lots of peeps, assuming this is their everyday go-to card. Next up…

Full 3X & 2 cents each – My personal valuation

I only put my travel and dining purchases on this card. And other purchases on other cards. So here’s how it breaks down if you’re in my boat.

You’d need to earn 22,500 Chase Ultimate Rewards points. And you’d need to spend $7,500 per year on travel and dining to earn that many. That’s $625 a month on travel and dining, which is super manageable if you eat out and travel even semi-regularly.

The CSR is a better deal for my travel and dining habits

The card shines when you make use of the bonus categories and get high value from your points. And that’s before you factor in the lounge access, $300 annual travel credit, and all the other perks of the card.

If you spend a lot on travel and dining, I’d recommend springing for the Sapphire Reserve.

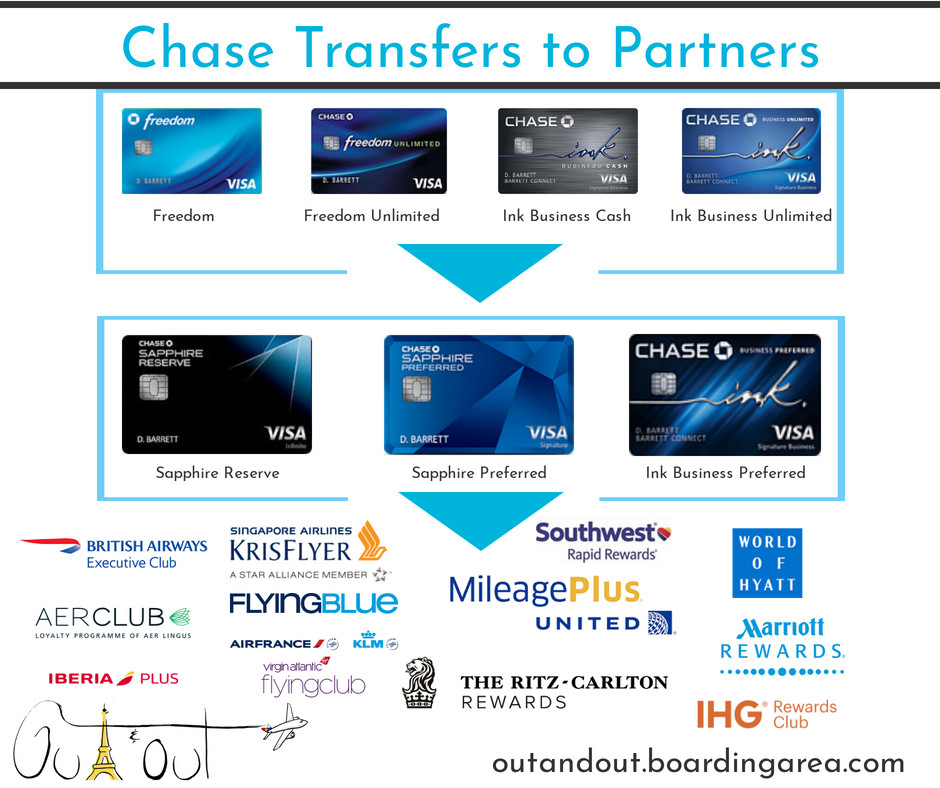

The list of travel partners

Your points can be worth so much when you transfer the points to travel partners. Here’s how I recently got a $2,000+ vacation to Puerto Vallarta for $90 using Chase Ultimate Rewards points.

Bottom line

- Link: Chase Sapphire Preferred – Compare this card

- Link: Chase Sapphire Reserve – Compare this card

As with everything points-related, the answer is subjective. However, most peeps will do well to keep and hold the Sapphire Preferred for the long-haul. And those who are moderate to big spenders in the bonus categories should probably grab the Sapphire Reserve.

In either case, it’s almost always worth paying the annual fee – because once you do, the rest is free travel banked right to your account.

Keep in mind, you can always product change from one to the other after a year, like I did. And you can’t earn the bonus on both cards or have both at the same time. So once you choose, you can cancel or change the card down the road.

I must mention you will NOT be approved for either card if you’ve opened 5+ cards in the last 2 years. But either card is an excellent place to begin if you’re new.

Finally, with the Sapphire Reserve, my calculations do NOT include the huge list of card benefits. But you can do well even without those in the mix, which goes to show how strong this premium card really is. It’s a nice step up, and a worthwhile card to hold long-term.

If you have either card, do you prefer one over the other? I’d also be curious to hear how you redeem and value the points you earn!

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

To be fair, you should add the opportunity cost of alternatively putting all that spend on a 2% cashback no AF card. Even this neglects the biggest opportunity cost, which is applying that spend towards a new signup bonus. I will be downgrading my CSR soon.

Thank you for saying that! I’m actually working on that post right now. The issue is: points valuations are subjective while 2% cashback cards are always fixed.

Of course, I completely agree the best way to spend is to earn a sign-up bonus. This post is for peeps who want to get a card and stick to it long-term. And your observation totally illustrates how subjective it all is. We love geeking out on this stuff but others just want a “pick one and stick to it” plan.

Are you going back to CSP? Or downgrading to a different card? Would love to hear your spending/card plan! Thank you so much for reading and commenting – I really appreciate it!

My plan is to downgrade my CSR to a CFU, and preemptively transfer my URs to Hyatt. Then in December I will upgrade one of my current CFs to a CSR and double dip the travel credit (I’m hoping if I upgrade a different card then I will get a new travel credit for this year, and another for 2019).

The CFU is on my dream list. I wish I could get it so badly. Excellent plan.

The CSR’s annual travel credit based on cardmember year now. So you can get it for 2018, and again in 2019 when the annual fee is due again. You can use the travel credit, then cancel the card to double dip like you said. Just keep an eye on the one-year mark and be sure to downgrade right when it hits so you can get the annual fee back.

I’m seriously wondering if I should spring for the CFU in place of my current CF. Need to run the numbers. Thanks again for commenting, and the food for thought. 🙂

You shouldn’t just be looking at the break-even point at which points earned negate the annual fee. You need to consider how much that spending could have earned on a no fee card.

For your CSP example of $1,188 travel +$2,375 other spending just to break even… that would have been worth $71 on a no fee 2% back card…

The no fee example works if you want to redeem for a statement credit, or even to book travel. But doesn’t hold up as well if you intend to transfer your points to travel partners, where points are often worth much more than 2 cents per point and can justify paying an annual fee.

But it’s definitely a thought to consider, especially if you just want to redeem for a statement credit – I agree than a 2% cashback card would be better in those situations.

The other thing to add is the Chase Sapphire cards have travel insurance, purchase protection, and their own shopping portal, which you can access when you pay the fee. And those perks are also very subjective and make the comparison even more convoluted.

Thanks for pointing this out! I 100% encourage everyone to look at all their spending and goals before deciding whether an annual fee is worth it. Thanks again for reading and commenting.

Hey, thanks for the clear comparison. This helps me justify sticking with CSP, whose $95 AF I just paid last month. I had originally PCd CF to CSR as I had no hope of ever getting a Chase card that was governed by 5/24. Then, when my Fairmont Visa automatically became CSP, I PCd the CSR back to CF. I figured if I really wanted CSR again, I could PC after the first year. I mean, CSP was free, so why not just enjoy it?

I don’t drink, eat out very little, and have a preference for quick serve places that accept Apple Pay. That’s key, since I love easily earning 4.5% with Altitude Reserve. I almost never use lodging that doesn’t have an associated CC; and with airlines, I’d rather get 5x via Amex (or 3x via Prestige if I’m booking on an often delAAyed carrier and could use the better protection). So that basically means rental cars (less than a handful of times a year, and always at cheap rates), parking (almost never) and tolls (never). I have a hefty Uber balance since GCs are always at least 10% off, and Lyft goes on AR since it’s Apple Pay. As do Uber Ride Passes (since they can’t be bought with credits).

Now it’s true that 3x UR > the flat 4.5% that AR offers. But there’s also much to be said for the simplicity of AR. Just type REDEEM after a travel purchase (or heck, setup a text replacement phrase like rm so you don’t even have to type the whole word!)…and, boom. Instant statement credit, days before the actual charge posts. This makes a huge difference compared to the CSR for folks who typically book domestic and will have to struggle to find fares that aren’t Basic Economy (if they want to use the portal to redeem UR at 1.5%). Not that I’d generally recommend using UR for that purpose, but I daresay that’s what most are doing. Partner transfers are just too complicated for the average person. Heck, even most highly intelligent people get lost trying to understand what we take for granted. But, I digress.

Back to CSP v. CSR. I decided it’s basically a FOMO situation. Yes, I feel a wee bit of jealousy those super rare times I see someone paying with a CSR. I’ve even been known to slide my CSP under theirs when splitting so they might assume it’s also a CSR. 🙂 Yeah, that’s pretty darn silly. But paying a $450 AF when I’m spending relatively little would be way crazier.