Also see:

I haven’t fallen off the earth or anything like that. Real estate in NYC is heating up, and my past few days have been pretty crazy with gearing up for the busy summer season.

I still intend to post the remaining 2 reviews from my recent NOLA excursion and have a few other things in the pipeline for ol’ Out and Out. And of course I’ve been keeping up with the latest points and miles news.

And here is a post in which I clutch at straws.

REDbird Part 2

Boo hissss

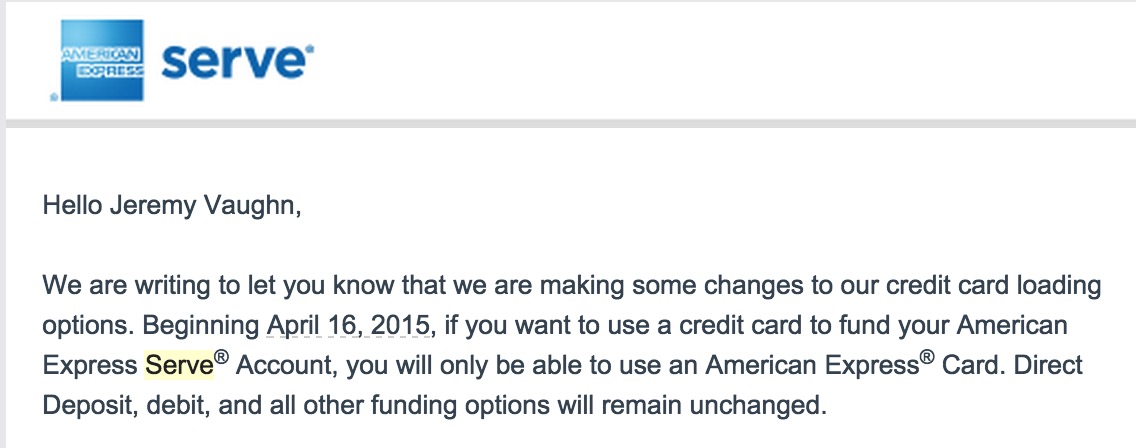

After having a terrible time reloading the REDbird card at my local Target in Brooklyn, I brutally dumped it and opened a new Serve account.

So, I was pretty dismayed when I found out they were going to restrict credit card reloads to only include American Express cards starting April 16th.

“Manufacturing spend” in New York City is already hard enough, and this is definitely an added blow. But there are 2 things I can find here that still might make Serve worth it for some people.

1. Even without earning points, this is a great way to pay bills that would not otherwise accept credit cards

2. There are at least 2 Amex cards that are NOT issued by American Express that may still earn points

The first point. Although there are better ways to pay rent than with Serve, if you need to float your payments through a charge card for a month or so, you can still use your Serve account to pay your bill and give you a little extra wiggle room, which could help a lot with cash flow from month to month.

The second point. It is up to the individual card issuers about whether or not to issue points for a purchase. American Express has decided they will not issue points for their own credit cards. But what about Amex cards that are not issued by American Express?

FIA and Citi + others

Two that I can think of right away are the FIA Fidelity Amex and the Citibank Platinum AAdvantage Amex. Both banks do not currently impose cash advance fees for Serve reloads (someone correct me if I’m wrong here), and both banks should continue to issue points since the reloads code as a purchase.

American Express may not give you points, but FIA and Citi still might. And this might continue to be a good way to get either 12,000 AAdvantage miles per year for minimal effort or $240 free dollars contributed toward an IRA with Fidelity.

Then, going back to the first point, you’d still earn miles and/or points for loading up your Serve card, and then can pay rent, student loans, mortgage payments, etc. to merchants who wouldn’t otherwise accept credit cards.