Update: This offer is no longer available. Check here for the most current card offers.

For my first Honest Review, I’ll come to a card I haven’t written about yet: the Chase Sapphire Reserve. Make that THE Chase Sapphire Reserve.

I’ve avoided mentioning it because, well, most of us can’t get it because of Chase’s prohibitive 5/24 rule. But, if you’re new to the points & miles world, wow. What a great place to start.

Or, if you can manage to get yourself a pre-approval in-branch (no dice here!), definitely pick it up.

You can tell if you’re really pre-approved is if Chase gives you a definite APR. If they give you a range, you’re pre-qualified, not pre-approved. You want that definite number.

The Chase Sapphire Reserve is in here, or at least you’d think judging from the publicity

Another strategy would be to say screw it and apply anyway. If you’re denied, have another Chase card waiting in the wings that isn’t covered by 5/24, which are at the time of writing:

- Chase British Airways

- Chase Hyatt

- Chase IHG

- Chase Fairmont

- Chase Marriott Business

- Chase Ritz-Carlton

That way the inquiries will hopefully combine and hey, at least you’ll have something.

The short

An all-around stellar travel credit card with huge rewards, an eye-popping annual fee, and a long list of perks that make it more than worth its weight in proprietary metal.

The long

- Link: Honest Reviews

In exchange for the $550 annual fee, you’ll get 4 or 5 times that amount back (or more!), depending on how you redeem your points.

This card is a game-changer because right off the bat, your points are worth 1.5 cents each when you book travel through Chase.

Good job cooking this one up in those headquarters of yours, Chase

So you’re already up to $1,500 with the sign-up bonus of 100,000 Chase Ultimate Rewards points after spending $4,000 on purchases within the first 3 months of account opening.

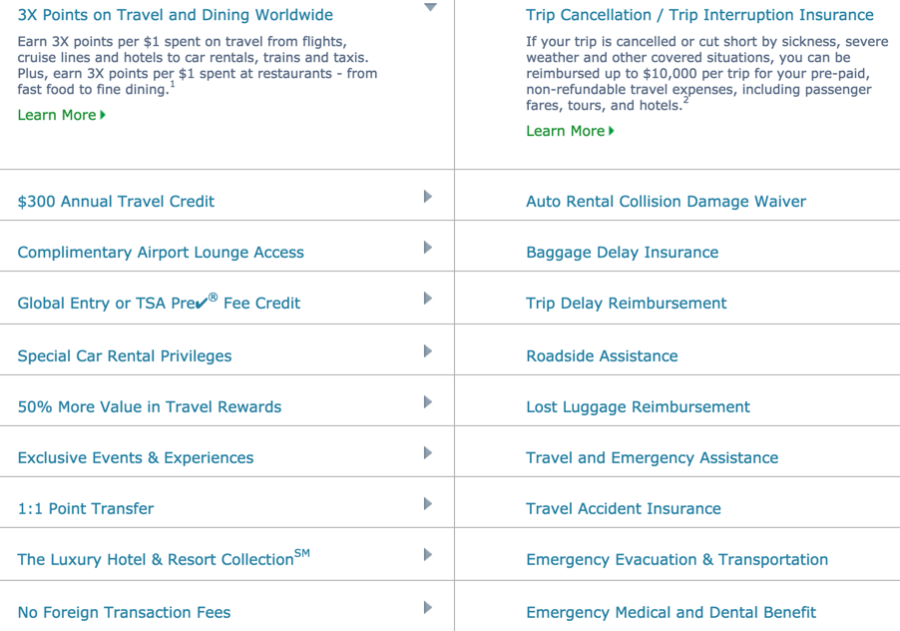

- $300 annual travel credit that resets after the close of your December statement

- 3X Chase Ultimate rewards points on travel and dining

- Priority Pass Select access with guest privileges

- And lots of other bennies that might come in handy one day, like roadside assistance, emergency medical evacuation, trip delay and cancellation coverage, and 90-day price protection – for starters

Chase Sapphire Reserve travel bennies

There’s been much spilled digital ink over this card. If you want it, check your pre-approval status in branch, or perhaps throw a random application out and see what happens – if you have backup or can absorb the credit inquiry within an overall app-o-rama.

That $300 statement credit tho

If you get the card in 2016, you’ll get $300 in travel purchases credited back to your account this year. And that’ll reset after the close of your December statement.

So in early 2017, you can hit it up for another $300 in credits.

In my mind, that erases the annual fee completely the first year. And you still have that 100K sign-up bonus. With $600 in credits added in, the total value rises to $2,100 – at least.

Grade: A

Kudos, Chase. You knocked it out of the park. Everyone wants with card and you claim you didn’t even market it!

You messin’, Chase?

This card is bold, now industry-leading. 3X is a new standard for travel and dining.

And 1.5 is the new base valuation of your points. And the $300 statement credit is the highest there is (I’m looking at you Amex with $200 on the Amex Platinum Card and you Citi with $250 on the Citi Prestige).

Normally, A stands for “Are you freaking serious? Why haven’t you applied already?!”

But for Chase cards, be sure to assess your situation carefully if you’ve had a lot of cards in the recent past.

Keep or DTMFA: Keep.

Is it worth paying $550 after the sign-up bonus is used up and the $300 statement credit’s been had? I think so, if only for the 3X category.

If you spend a lot in those categories, you’ll rack up a mega amount of points throughout the year. And considering each point is worth 1.5 cents, that’s 4.5% back toward travel on those purchases.

$10,000 is a low figure for lots of peeps in the travel and dining categories, especially if you have a lot of paid airfare, tolls, bus and subway passes, hotel or Airbnb stays, or if you eat out a lot. In that case, you’ll earn a huge amount of points of the course a year, which makes this card a firm keep, annual fee and all.

Do you agree with my assessment? The Honest Reviews series is new, so I’d love to hear your thoughts to shape the column moving forward!

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

New fan of your blog. Great review, looking forward to what’s ahead.

New fan of the blog. I’ll pop in from time to time.

Thank you, Brian! Please do – and thank you for reading!

Your assessment at the end where you said you’d need to spend $10,000 to cover the annual cost is a little off, since you get the travel credit AND 3x the points on travel and dining. So after the $300 travel credit, you’d also have 900 points, which is worth $13.50. That leaves $136.50 of annual fee to cover. If all your spending was travel and dining, you can close that gap by spending $3,033. The MOST you’d need to spend to cover that remaining $136.50 is $9,100, but that’s assuming $0 spent on travel and dining after the travel credit.

I like your logic!

With the $300 annual travel credit, the numbers become even more favorable for sure.

Thank you for adding this and breaking it down so clearly!

Sorry to necropost.

I haven’t quite worked this out, but I’m not sure the math is as easy as Mike put it. Yes, you can make up $150 in points by spending $5,000 on travel (or $136.50 by spending $3,033), but it’s important to remember that you’re not comparing this card with nothing. You’re comparing it with other offers.

For example, the (non-Reserve) Sapphire gets you 2x points for travel and dining without an annual fee. That means that your net $136.50 annual fee is really only getting you 1 extra point per $1 spent on travel and dining. In order to make that worth it, you need to spend at least $13,650 a year on dining and travel just to break even. (I’m probably leaving out other perks of the Reserve.) If you don’t spend that much, you’d be better off getting 2x points with no fee on the non-Reserve card.

And if you are a couple, remember that there’s an extra $75 annual fee per extra user on the account. That’s another $7,500/year in travel and dining. Crap. I think I just convinced myself to cancel the card after the first year… Maybe I missed something.

(Of course, if we’re worrying about $75-100 when we spend over $10,000/year on travel and dining, maybe our priorities are off.)

I definitely agree with this review. You net $150 from the 2016 and 2017 travel credit alone, but it’ll be hard to decide if I should keep it come next fall when the fee is due again!

I think the bonus categories are worth it alone. It will also be interesting to see what Chase adds – or takes away – in the next year or so. Those could potentially be game changers or deal breakers. But it’s definitely worth getting right up, that’s for sure!