Also see:

- Dear Amex: DIAF!

- American Express Vs. Chase: Why Chase Is Winning

- Booking Barcelona: $747 Round-trip in AA Business Class

- Citi Offers to Compete With AMEX Offers “Soon”

And, bye EveryDay Preferred, hello ThankYou Premier?

Recently, I’ve seriously been pondering why it is I hang on to my AMEX cards.

I’ve had at least 2 since 2012, and haven’t accumulated enough points to actually do much.

Membership Rewards… meh.

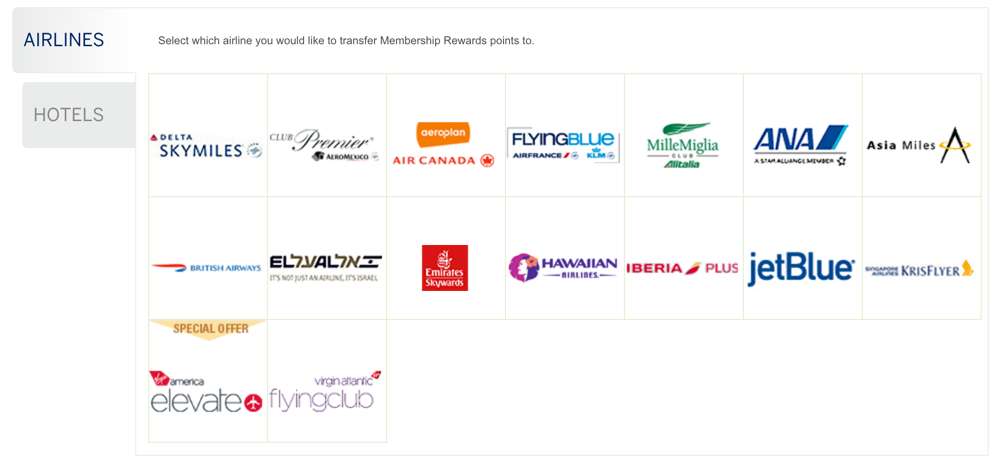

I’ve always thought there might come a day when I’d finally transfer some AMEX Membership Rewards points for an award booking on ANA or Aeroplan.

Are any of these useful… or nah?

In particular, you can fly to Western Europe for 45K miles each way in business with Aeroplan, or 90K miles round-trip (until December 14th, 2015).

That’s changing in about a month. On December 15th, 2015, the price will increase to 110K miles round-trip for a partner award flight in business class.

There aren’t too many other sweet spots that rival other Star Alliance carriers.

Fine, what about ANA? The biggest upside is you can string along a trip with lots of stopovers.

I haven’t exactly been following closely because they change their award chart and routing rules so frequently.

But redeeming miles is always about the best deal you can get at the time of booking.

Again, I’ve always been curious about ANA and Aeroplan, but I’ve never had 110K (or close to there) to actually book an award. So, meh.

Look at this little collection of uselessness

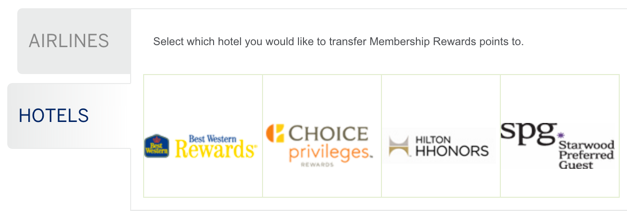

And the hotel transfer partners? SPG, nope (bad ratio of 3:1). Hilton, nope (a waste when you could transfer to an airline partner instead). The best one is actually Choice Privileges!

But because I have Chase Ultimate Rewards, I can access Hyatt and I already have plenty of Hilton and IHG points, so…

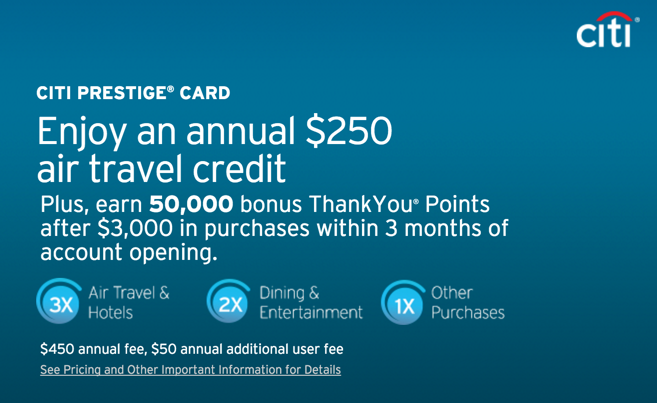

And, Citi Prestige encourages paid stays, which I’ll get to in a bit.

Why keep the Platinum Card?

The AMEX Platinum Card is almost legendary for its long list of perks. You get:

- Starwood Gold elite status

- Hilton Gold elite status

- Lots of car rental status

- $200 airline credit on an airline of your choice (most large domestic carriers are on the list. American, Delta, United, Southwest, etc.)

- Access to Fine Hotels & Resorts for late check-out, spa and dining credits, and possible upgrades

- FREE CENTURION LOUNGE ACCESS

- Lots of other ancillary benefits

The 2 perks I’m most interested in are the $200 airline credit and Centurion Lounge access.

I’ll do a proper post about this, but I’m closing next month on a house in Dallas. I’m not sure what that means yet (I’ll work out those thoughts in the post), but it seems the biggest perk – for me to keep or lose – would be the Centurion Lounge access.

Here’s my completely gratuitous review of the Centurion Lounge @ DFW.

Ah, craft cocktails at the Centurion Lounge, how I’ll miss you. Ah, huge crowds and the fight for a seat, how I won’t

The $200 airline credit is great, too.

I’ve been known to buy $50 American Airlines gift cards and/or buy lots of beers and liquor whilst sitting in coach. And this is nice, no doubt.

But…

Why get Citi Prestige?

Citi Prestige, you alluring little thing.

This card comes with its own laundry list of perks that make it worth its ilk.

The face of intrigue

The biggest perks I can see are:

- $250 airline credit to use on ANY airline for ANYTHING including airfare

- Points-earning of more than 1X! Take that, AMEX Plat!

- Admirals Club access when flying on American

- Priority Pass access for you and 2 guests or immediate family – for no extra charge (AMEX’s version charges $27 per guest)

- The 3 free rounds of golf benefit (not for me, but definitely for some! Golf is expensive!)

- 4th night free on pretty much any hotel stay AND you get to earn points, have elite status recognized, and stack discounts

Now, I already get my lounge access to Admirals Club for free thanks to Business Extra, so this is a moot point for me. Although it would be nice to use the Business Extra points for award flights instead.

And I’d definitely use the Priority Pass access.

The biggest perks for me would be the 4th night free on hotel stays and the $250 airline credit.

Also, you actually earn points that mean something. You can redeem for miles-earning flights on American, and each point is worth 1.6 cents each. And:

- You’ll earn 3X Citi ThankYou points on airfare and hotels

- And 2X Citi ThankYou points on dining

That’s essentially a 5% discount or 3% discount on American (1.6 x 3X points is 4.8 cents for airfare and hotels, and 1.6 x 2X points is 3.2% from dining).

Plus, Citi ThankYou points transfer to FlyingBlue and Singapore Airlines, which duplicates AMEX Membership Rewards (and the Virgin duo of Atlantic and America). Those are the biggest upsides, IMO. I really wish they’d add a meaningful domestic carrier, but that’s another post, too…

EveryDay Preferred Vs. ThankYou Premier

When AMEX came out with the EveryDay Preferred card, they accidentally created the best Membership Rewards-earning card, which is kinda tragically hilarious.

It earns

- 3X AMEX Membership Rewards points at US grocery stores, up to $6,000 per calendar year, then 1X

- 2X AMEX Membership Rewards points at US gas stations, unlimited

- 1X AMEX Membership Rewards point everywhere else

But the kicker is that after 30 transactions in a month, you earn 50% more points, so 4.5X on groceries, 3X on gas, and 1.5X everywhere else.

I like that last bit: 1.5X everywhere else.

It’s almost not enough though. Too little, too late.

Combined with some not-so-great transfer partners, you really have to cherry-pick your award redemptions.

- Delta still offers some great prices for awards on Virgin Australia and Korean Air

- Singapore is great, but as mentioned, duplicated with Chase UR and Citi TY

- Aeroplan and ANA for specific uses

The others can DIAF, especially since British Airways announced the devaluation of short-haul flights and AMEX sliced the ratio to 800 BA points per 1,000 AMEX points.

(Although Iberia Plus might be a saving grace. But I have their points via Chase UR and I can get to Australia or Asia with American miles.)

But for the $95 annual fee, Citi ThankYou Premier takes it on.

You get:

- 3X Citi ThankYou points on ALL travel, not just airfare and hotels

- 2X Citi ThankYou points on dining

Man, I wish Citi would switch up the categories on the card. But whatever, I can use my Chase Ink Plus card for gas. The only category I’m losing out on is grocery stores, but it’s not a huge loss. So many other cards earn points at grocery stores.

Bottom line

Both AMEX and Citi have a card with a $450 annual fee, and a card with a $95 annual fee.

Blow for blow, I think the Citi cards take on the AMEX cards well.

And after my devastating recent interaction with AMEX that cost me hundreds of dollars, combined with several other “bad taste” encounters before, I’m thinking of dumping the AMEX Platinum Card, and downgrading my EveryDay Preferred to its no annual fee version just to keep access to AMEX Offers (although Citi is supposed to release Citi Offers for You… soon).

My biggest loss from dumping the AMEX Platinum Card will be the Centurion Lounge access, especially as I consider basing myself at DFW.

But on all other points, the Citi cards handily overtake the AMEX cards point by point… literally.

Competition is a healthy thing, and I’m glad Citi is taking AMEX on. I’ve always said, when banks compete, you win.

I think I’m going to bite the bullet and sign up for the Citi Prestige card. (And if you are to, thank you for using my links to apply!) I’m looking forward to exploring a new points program.

As for the EveryDay Preferred, it’s too little too late. And I’m feeling both underwhelmed with AMEX Membership Rewards and interested in Citi ThankYou points. It’s a perfect storm for a little switcharoo.

What do you guys think?

- AMEX Platinum Card or Citi Prestige?

- AMEX EveryDay Preferred or Citi ThankYou Premier?

- AMEX Membership Rewards or Citi ThankYou points?

All opinions valid, would love to hear your take on it!

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

You make a seriously good point about the decline of Amex. I know there will be many fanboys that hold onto their plat cards until the benefits dry up, but after being shafted by Amex a few times myself I really empathize with your post.

I survived a FR with seriously reduced limits on cards that weren’t involved in the spending or even linked on the same account that had also been opened for nearly 15 years. While the charge card that I had made the $5k in spending over 3 days (legit spending, remodeling house) was left completely alone. So Amex essentially slashed the limits on the card that I make the most transactions on ultimately forcing me to move transactions onto my chase lineup. I wasn’t about to pay down my balance multiple times a month.

That coupled with a more recent change in how the 30 transactions a month are calculated on the Amex Everyday Preferred card, I’ve been having a harder time qualifying because it seems like Amex just picks and chooses which transactions count. In addition I no longer am targeted for any good Amex Offers (likely due to the FR) I just find it harder and harder to justify keeping my business when them.

They were the go-to, the best point earner but if those points continue to be worth less and less, and like you my intention was to use them to book a nice ANA trip but I am nowhere near the miles needed, I just can’t keep holding onto them.

The only redeeming hope for Amex was a recent purchase protection claim which they didn’t even blink an eye on. I’d be really curious to see how easy the process is for Chase. If anyone has any experience let me know.

Otherwise I’m seriously considering dumping Amex and moving to a Chase/Citi combo.

Dude, sounds like they’ve put you through the wringer.

If I dump AMEX, I’d essentially be moving to a Chase/Citi combo (with a few random cards here and there.)

I can’t really see what I’d be missing out on any more. Yes, AMEX cards definitely have their fanboys, and it will continue to be worth it for some people, but I think I gotta move on.

I try hard to use my cards for regular spending and “be a good customer” but the AMEX relationship has been one-sided except for the lounge access and AMEX Offers.

Which is why I’m excited about Citi Offers for You (when it finally comes out) and the fact that the Citi Prestige card will offer lounge access anyway.

If AMEX ever puts me through a FR, I’ll simply cancel the cards. Not worth it.

Citi Prestige is looking better and better. My AMEX Platinum renews this month. At this point, I think I’m gonna make the leap. Plus I’ll earn more points on regular spending with the Prestige.

Thank you for sharing your story. Glad I’m not the only one observing the gradual decline.

Btw I’m a Dallas local too!

Ah, nice! Say hello if you ever see me out and… uh, out!

LOL 🙂

I tend to agree – will be a tough decision when comes time to decide between the two, but i’m not going to pay to continue holding 2 $450 cards. One thing to note – the Premier actually includes gas at 3x (better than the Prestige), so wouldn’t necessarily need to put it on Chase Ink Plus. And welcome to Dallas!

Thank you Matt! Are you in Dallas? So excited for the next step, whatever it ends up being!

Such a funny quirk about the Citi ThankYou Premier card – it actually has a better points-earning structure than the Prestige.

I’m not totally sold on having both long-term, but I’ll definitely keep it for a year and see how it goes.

Seems like gas is covered. Only category left to cover is groceries, then EveryDay cards can be phased out.

I have the Everyday Preferred, and I chose the cash back option instead of the points. I have a hard time getting value from Amex points (unlike the rest of the free world), so 6% back on grocery stores and lots of other stores (cause they sell gift cards at grocery stores) works best for me. The fee on that card is only $75.

6% cash back is definitely a respectable rate of return. Feel you about getting value from AMEX points.

That’s what I love about having so many credit card options – you can customize your selections to suit your own patterns.

As long as you’re getting more than $75 cash back a year, it sounds like you’ve worked out a good strategy!

I have both Amex Platinum and Citi Prestige + Premier. Will dump Amex Platinum and might keep the Prestige. I’ll also keep Amex PRG and Citi Premier.

The Citi cards are competitive with Amex, of course. The people who work for Citi are very smart and have analyzed what Amex offers …

Yes, agreed. I didn’t get much use from my PRG and the annual fee just wasn’t worth it.

Very interesting back-and-forth with these cards though. They definitely know what they’re doing and I’m thinking Citi has the upper hand at this point.

“but it seems the biggest perk – for me to keep or lose – would be the Centurion Lounge access.”

Would you *really* use this perk all that much of you live there? Miami is one of my home airports and I *still* haven’t been in the centurion lounge there once. When I am departing, I arrive only a short time before my flight (maybe an hour or so) and then get on my way (and I fly Delta, so the lounge isn’t all that convenient anyway). And then when I arrive home, I want to GET HOME, so I leave the airport immediately. I find that I use lounges mostly at transfer points and sometimes at final destination to shower/clean up before getting to my destination.

Finally, most of the time, if I hang out in the lounge, I also have to pay for extra parking fees that usually accrue by the hour when over the day limit.

Hey Mark!

The AMEX lounge @ DFW is located in Terminal D, and most American flights are from Terminal A, but not all of them. Others ARE from Terminal D. I’ve been lucky enough to walk out of the Centurion Lounge to the gate without dealing with the Skytrain my past few flights.

You make an excellent and valid point. To break even on the $450 annual fee, I’d have to visit 9X times a year (assuming each visit is worth $50). Or 5X a year if you factor in the $200 airline fee credit. Which is do-able.

But the thought of paying for 2 cards with a $450 annual fee – $900 total – seems overkill. Unless you travel A LOT.

I guess it’s one of those weird things. I know it’s “just” a credit card, but I’ll miss it, and visiting this particular lounge from time to time.

But at the end of the day, a few visits to one lounge isn’t enough to justify a huge annual fee on a card.

Harlan, perhaps ignore my earlier reply. If you downgrade to the Everyday — I assume it will be at no cost.

So, since you never earned a bonus on THAT CARD, would you not be eligible for a bonus by taking out a 2nd Everyday Card, since on the earlier no bonus was ever earned???

I’m not schooled on the ins and outs of AMEX bonuses, but I thought that the once in the lifetime bonus was applicable, if indeed you actually earned a bonus for taking out that card!

Since you only earned it for the Preferred Everyday — and I do believe that they are considered different products — would you not be eligible for the bonus when and if the increased bonus is offered???

You’re right! You can only earn the sign-up bonus on any AMEX card once per lifetime, and the 2 “EveryDay” cards ARE considered separate products.

I’m good until March of next year (that’s when the AF is due), so I might apply for the EveryDay and cancel the EveryDay Preferred.

There are a couple of strategies, but nothing urgent. I might hold out for a bigger sign-up bonus.

Good for you!

Also, timing may be your friend, then, as well!

AMEX should be going thru its death throws with respect to the Costco account at about that time, and they may wish too keep you as a customer for the EDP — drive a hard bargain with them, and if they say no, then say enjoy yet another card member loss to your portfolio — I know I am but a small fry, but all us small fries add up to something huge ON TOP OF YOUR LOSS OF 10% OF YOUR CARD MEMBERS AS A RESULT OF YOUR LOSS OF THE COSTCO ACCOUNT!

You can add that they might very well be soon be choking on all that plastic that is coming back to them — figuratively speaking.

LOLOL, love it! The timing is pretty impeccable. I’ll use my best negotiation skills with them in March 2016. 🙂

Harlan, I generally agree with you and I guess that the AMEX Everyday Preferred is a good card if you want to earn MR points — but as you have noted above, the sweet spots for MR redemption are a fast diminishing!

So, who want to earn more of a restricted currency???

Better to save what you have and keep it from being turned to dust!

That’s why the single best AMEX MR earning card out there is the NO FEE AMEX EVERYDAY card!

Wait for a decent bonus, if you can wait, and if not, pull the trigger and PRESERVE all your MR points without worrying about spending them willy nilly when you cancel the Platinum AMEX card.

Then take advantage of those AMEX offers selected for your Everyday no fee card and spend your MR points at your leisure!

Yes! I have an EveryDay Preferred card now that I’ll simply downgrade to a no annual fee EveryDay card, to keep the points active AND transferable (for those oddball transfers maybe).

The question is, do I wait for a bonus or just downgrade because the bonus is usually only 10K points…?

As always, I love to hear your opinion. Thank you!

Try the incognito trick to get the 25,000 point bonus if it is available. Not sure, if you have to make a decision now, but since the 25,000 bonus is so much better than the regular one, and if you have to bite the bullet and do something to keep those points active, I would say either to get a new MR points earning cards where the first year would be free — PRG card??? — or bit the bullet and keep the Everyday Preferred and wait for the bonus on the Everyday to jump at some points — apply for that card once it does, and then cancel the Preferred Everyday and get a Pro Rata refund.

I have to think that a Pro Rata refund of a $95 annual fee card –?? — is a whole lost easier to swallow than a $450 Plat AMEX card, even allowing for the $200 calendar year return on gift cards, etc.

So, yes, I would wait it out and jump at a higher sign up bonus for the Everyday – cause 15,000 extra MR points are nothing to sneeze at — even if I don’t value them all that highly, as opposed to the rather small OOP cost of biting the bullet and temporarily paying the annual fee for the Preferred — with the hope that some of that will be returned as a pro rata refund when the Everyday offer jumps again.

Good luck!

Excellent ideas and analysis as always. You’re right, 15K points is certainly better than none! I’ll wait until early next year to figure it out. But I DO know that for now, the AMEX Platinum Card has to go!

Could not agree with your more about the AMEX Platinum — BUT — I seem to recall that you may have another 60 days from a certain date to get a full refund of that card.

If so, then you might wish to hold onto it — if the timing works — to eke out another $200 in airline fees for 2016.

Not sure if it is doable, but it might be.

Also, even if you can’t get the full cash back within 60 days, it might be worthwhile to wait and reap the 2016 airline fees and then go for a pro rata refund — you still might come out ahead — not sure — but consider this possibility.

Excellent and valid point. I like the way you think!

I still have the ol’ sucker yet, I might just squeeze out all the value I can toward flights on AA with $200 in gift card purchases.

You know I get impulsive lol. Thanks for being the voice of reason yet again! 🙂

I also made the transfer from Amex to Citi. Now I have the Prestige and Premier and only the Everyday no fee version.

There are a couple of airline partners I do wish I had from the Amex list, but like you I have yet to run into the need to use them over an alternative.

Also, I’m mostly abroad so having a card with no foreign transaction fees is big.

The only thing left to figure out is what card to use on groceries (especially abroad). May just look for gift cards at places bonused by other cards (like the two Citi cards).

Wow, sounds like we’re on the same card system now. Great idea about the gift cards.

I get most things from Costco and they’re not considered a “grocery store” but I save so much money there that I’m fine with earning 1 point per $1 (on whichever card I end up using). I can actually get 2% cash back there now with the Fidelity AMEX until they switch to Visa in March 2016.

I only go to grocery stores for little this ‘n’ that items, so it’s not a huge category for me. I’ll get a strategy together soon enough, I’m sure.

Glad to hear others have made the leap over to Citi. They’re definitely doing a lot to compete and attract new business. Looks like they’re getting me next!

do you think that TYP are going to be devalued soon….its just so easy…??

Personally, I don’t. Look at Chase UR – they have 5X categories with the Ink cards and still manage to keep their award program afloat. Will the individual programs devalue? Maybe. But I think it’s a solid bet for at least another year or more.

Plus they’re just ramping up the program, I don’t think they’d butcher it right at the beginning.

I’m a DFW hub captive with both the Prestige and the Amex Platinum.

You’ll be living in AA’s backyard. You have to have the Prestige. End of story. Obviously.

(Open a Citi Gold account and the fee drops $100.)

The question is whether you keep the Amex. On the lounge front, the first Mark above is 100% correct. I have, however, used the Centurion Lounge when flying Spirit, which also uses DFW as a mini-hub; Terminals D (Amex) and E (non-AA flights) are close.

My call: Amex is not worth it. I got mine for the 100K sign-up bonus and still have it because of a huge — very huge — retention offer.

So your path is clear. Get the Prestige. Reassess after a year.

(And do, please, open a Citi Gold account. This has to be on line; all bricks & mortar Citi branches in Texas vaporized this past March 22.)

Tom, thank you for the tips!

I was pondering a Citigold checking account, but the $30 monthly fee is kind of a turn-off. Seems like I’d be paying $360 to save $100 unless I link an account with a huge balance to it.

I might dump the AMEX Platinum and wait for a big sign-up bonus on the AMEX Business Platinum Card.

Good stuff to think about. Thank you!

Citigold also gets you 15% more miles each year. Similar to the Chase Sapphire Preferred benefit that went away.

Thanks for adding that. Certainly a nice added perk!

The Premier (not Prestige) includes gas with its travel bonus.

Yes, that’s an odd quirk. I’ll use my Chase Ink Plus for gas for the time being, as I find Ultimate Rewards points extremely valuable for award flights. Not a deal breaker by any means, but something to note for sure.

Thanks for reminding!

Harlan —

Wanted to points something out about your new Citi Premeir card that you may have not been alerted to —

YOU EARN 3 TY POINTS/$ FOR GAS!!

Gas is treated as transportation/travel for the Citi PREMIER card, and since you are moving to Big D — gassing up likely will be in your future more than mass transit.

Don’t know what the benefit for gas purchases for the Citi Ink card is but the Citi Premiear earns you 3 TY points, so that is essentially like as you have noted above — ~ 5% cash back when use to purchase AA tix — which is not a bad thing to get since you will be swapping the Big Apple for the Big D!

Good luck on you closing!

Thank you so much. 🙂 I really appreciate the warm wishes, and always love hearing from you.

You’re right, gas will be a bigger consideration in the ol’ TX. I might just rely on Chase Ink Plus for now and add the Citi ThankYou Premier later. Baby step my way in, so to speak.

Excellent points for folks to remember though. Can’t understate the 5% toward AA flights! (Especially in Dallas!)

100% agreed with this article.

Good points! We picked up Citi Prestige and bagged our Amex Plat a few months ago when they started declining access to Centurion Lounge unless you have a seat assignment on boarding pass (translation: no airline employees on personal travel) We have no regrets! Plus, two free guests with Priority Pass is huge bonus for the Citi Prestige card. I was curious about Amex Everyday but you have now cleared that up. When the Amex/Costco deal ends, all of my Amex cards will be gone. (A year ago I had 4) I am kinda done with them. The competition has upped its game as Amex has rested and worked to alienate good customers.

Preach!

I may keep 1 no annual fee AMEX card only to take part in AMEX Offers.

The competition is working harder to bring value with their similar cards, and AMEX isn’t improving their offering.

I can’t believe the AMEX Platinum Card still only earns 1 point per $1!!!

Wish Citi Prestige would set up Gold Status with Hilton (seems totally plausible considering they issue Citi cards), or some other elite status offering.

But still, a mile better than the rest! Loving this card so far!

Just have to say that I have both the Prestige and the Platinum. But when my friends ask me which I prefer, it is the Prestige that I continuously push to them. The $250 credit towards airfare is huge! I know AMEX gives you the $200, but the gift card route is a pain, and technically, not allowed under the terms and conditions and can be shut down by AMEX at any time (it didn’t work for two months from August to October before being allowed again). If you have status with the airline, it is tough to spend $200 on booze.

Also, for me, the golf benefit is worth noting. I do golf, and I get three rounds at courses throughout the world for free. This includes some very expensive golf courses, like TPC Sawgrass (well over $300 per round at peak season). I am playing a course this Thanksgiving that would have cost me $110. All of these things and the fee is already paid for.