TL;DR: Had crappy credit. Used points cards as motivation to improve my credit score. Hooked ever since.

I’ve taken a server job a few nights a week to get out of the house, stay active, and be social. I see people using credit cards more than ever. I’m shocked by how many people still throw down debit cards. Most of them are millennials.

Google has the tea on millennials and CCs

My generation is a complicated story of student loan debt, job-hopping, delaying children, unable to afford or save to buy homes, living longer than ever – and definitely NOT wanting to get sucked into credit cards.

I see cool metal cards here and there – but most millennials are using well-worn debit cards from local banks.

If you can use credit responsibly and pay the balance in full every month, then you’re leaving money on the table by using debit cards. Even a 2% cashback card with no annual fee is free to use and earns literally free money.

I started college in rural Vermont – and promptly got into credit card debt

I remember the sting of credit cards: opened a student credit card when I was 18, charged textbooks I couldn’t afford, and fell into the soul-crushing cycle of debt. Such a slippery slope.

Then I did the unthinkable: defaulted on a student loan. I was so poor, making $120 a week working overtime at retail jobs. And they wanted $500 a month? I ripped up the bills and threw them in the trash. I didn’t have extra money. How was I going to come up with $500 more every month? And that was the “financially burdened” plan. 😑

Getting into rewards credit cards

6 years ago, I’d been at my first salaried job for nearly a year, making $36K annually as a Marketing & Communications Associate for a non-profit. I thought it was so much money at the time.

I got up at 7am every day to be on the F train by 8am. The ride took 45 minutes. And some days, I’d have time to pop into a bogeda on 61st Street and grab a coffee.

There was a Chase Bank around there too. I’d stop in to use the ATM. One day, it was broken so I had to go to the teller. He offered me an application for the Chase Sapphire Preferred card. My first thought was, “no way in hell I’d be approved.” On the way out, I saw the sign talking about 50,000 something-or-other points and had no idea what they were talking about – and it probably was all BS anyway.

This guy had no idea he was about to get a new travel hobby

No, I had my checks direct deposited and used a debit card for everything. Plus, I still had deep, ugly marks on my credit report from life’s follies: an unpaid electricity bill from when I lived in Buffalo, a library fine with interest for a book I’d returned 2 weeks late, defaulted student loans I tried to wish away. My credit score was in the 500s and I was positive there was no coming back from it.

But, I was curious about those 50,000 points.

You can Google anything

Later that day, I typed “50,000 chase points” into Google – probably expecting it to be full of scam alerts, ripoff reports, and how Chase was literally the devil reincarnate. Instead I ended up on The Points Guy, Million Mile Secrets, Frugal Travel Guy, and the other blogs around at the time.

When I found Chase points were actually super valuable, I felt like I was missing out. (And certainly had no idea I’d be writing my own version of how to use 50,000 Chase points one day!)

I also knew nothing about airline loyalty, upgrades, shopping portals, or dining rewards – there was a points system for everything. And holy crap, you can even get a whole vacation for only a few bucks. FML, I’d been paying for coach seats and resigned myself to the back of the plane. I’d never be one of those people who flew up front.

They made it all sound so easy. Plus, you needed good credit.

I closed all the browser tabs (probably at 3 in the morning after falling way too deep in it). But I kept thinking about it…

Getting my credit right

- Link: Credit Karma

- Link: Credit Sesame

I did something long overdue. I knew it would be ugly. Probably a bunch of stuff I’d forgotten or didn’t know about. But I did it. I pulled my credit report.

(You can use a free service like Credit Karma or Credit Sesame to take a look. And you can order your reports from all 3 credit bureaus for free once a year at AnnualCreditReport.com).

It was all there, in black and white. The defaulted loans, the overdue bills, the old credit card I used to buy textbooks, all of it. With numbers and due lates and codes of how behind I was. And over it all, a pathetic number like a grade hovering above it all – the credit score.

I rarely used sick or personal days. So, I took one. I fired up my phone and started dialing all my creditors. With such a pit in my stomach.

I thought the voices on the other end would scold me. Give me speeches I didn’t want to hear. Or make me feel bad about slipping so far and for so long.

Instead, I found people that wanted to work with me. Many of them offered payment plans or settlements for much lower than the original amounts.

I asked for proof in writing that I’d paid the debt – that it was done, once and for all.

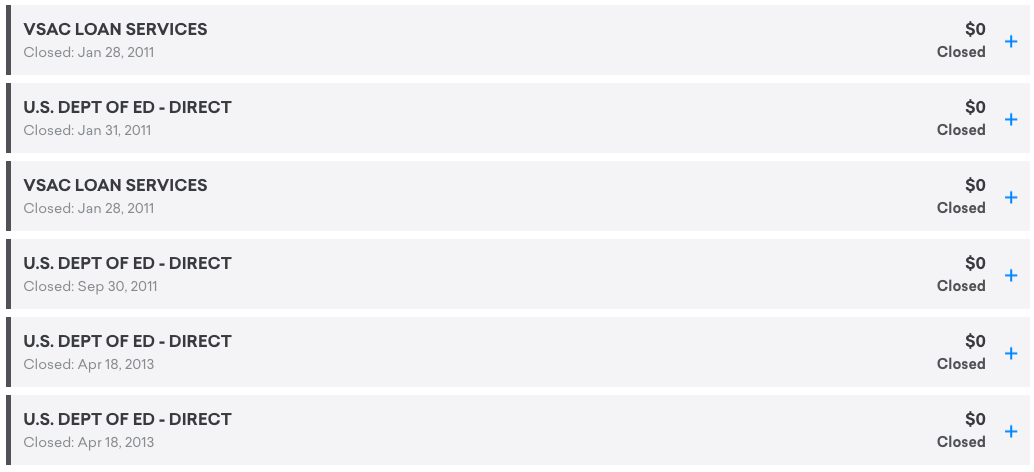

Then I went for the Big Kahuna: the freaking federal government with my defaulted student loans.

“Wow,” the girl said as she opened my file. (I imagined cobwebs and dust flying off the screen.) “You should’ve called us a long time ago. We have so many new plans now.”

“I know, I know…”

My student loans are still a thorn in my side, but I’ve learned to live with them

So here’s what happened: the loans had gained so much interest. That will never go away. I still have to live with that. But they were updated to an active status. I got on the income-based repayment plan (IBR). My new payment was much lower than expected. I just had to prove my income once a year.

It took ~3 months for the loans to update on my credit file. And for the other bills to fall off or show as paid in full. But, one by one, they were all fixed. I only had to call 1 of the creditors to follow up.

And soon after, my credit score started jumping – each week it seemed higher.

Back to Chase

- Link: Chase Sapphire Preferred – Compare cards here

I still wanted that Sapphire Preferred card. In those months, I thought of it as a symbol of a new era. (I still think it’s the best card for beginners.) So I went back to Chase and spoke with a banker. This time, I was pre-approved for the Sapphire Preferred card. And did I want to apply?

I almost did it. But I was still so unsure. If I was gonna get a denial, I wanted it to be at home, so I could feel disappointed in private.

When I got home that night, I fired up the application. And got an instant approval! I couldn’t believe it.

After all the calls, payments, and months of watching my score, I was finally able to pull myself up enough to get a premium rewards card.

I couldn’t wait to use it for everything and get that big sign-up bonus. It came in the mail the following week.

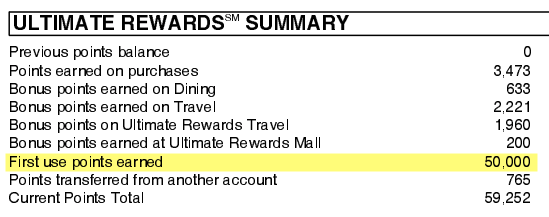

From my first Sapphire Preferred statement

I used the card for everything. And paid it off religiously. The points kept rolling in: between the card, dining programs, shopping through the portals, and keeping up with the promotions, I was soon rolling in Chase points.

Before I knew it, I took my first award trip to Hawaii. And in March 2013, Out and Out was born to record my adventures.

I went back to Hawaii in 2016 – and took my family with me!

From there, I signed-up for other cards to earn various sign-up offers, benefits like elite status, or just to have other bonus categories. I now have 30 cards! But it started with one – and started slowly.

The first step was to learn to trust myself to be responsible with credit. When you have that trust in yourself, you can earn points for pretty much every purchase.

Plus, with my good credit, I’ve been able to buy a home, get an automobile with a low monthly payment, and of course get all the best credit cards on the market.

Bottom line

The last 6 years have been a wonderful ride. I’ve been to destinations I’d dreamed about my whole life (Hawaii, Easter Island, Japan (twice!), and all over Europe). I love writing for my blog. And have met so many amazing people. (If you’re in Dallas, join my frequent flyer meetup!)

But it’s not like I started here. I worked my way up from the bottom of the barrel, using rewards cards as fuel to dig myself out of crippling debt.

After my first award trip, I was hooked. I still feel giddy when I book a cool trip using points.

But that’s how I got started with points & miles. Not even at the beginning, but several steps behind before I even began.

I still have those student loans. But I also have ample savings, bought a house, and get the best interest rates every time I borrow. Good money habits are just that – habits. Anyone can learn a habit.

If you love travel, maybe points can be your reason, too. I find having a credit card actually gives me more control over my cash flow. If you’re not into points, get a cashback card with a $0 annual fee – and get free money just for using it. There’s no need to ever use a debit card. Even for millennials.

What got you into points and miles? And if you don’t have a points-earning card, do you think you’ll ever get one?

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Great job Harlan!!! So happy for you! The Chase Sapphire Preferred was my first credit card too (well, i was grandfathered into it by Chase since they discontinued my previous credit card) and it was the only card I had for years.

To this day, I think it’s a strong card for introducing beginners to a points system. With regard to the hobby, I was amazed at how good my credit score became – and how much else I’ve been able to do because of it. I owe a lot to my interest in points & miles. Thanks so much for reading – I’m glad we got to meet back in the NYC days!

Glad the points and miles journey was successful for you.

I remember getting into points and miles when I first started my career eight years ago. I was also nervous about credit cards as a result from debit from college tuition, books, life’s choices, and only using debit cards for all purchases. An extremely useful tool I used to pay down the debit I accumulated was to take advantage of balance transfer offers with either 0% or 2% fee with 0% APR for 12-18 months through various credit cards. Years later, I paid off all of that debit and now travel to Asia and stay at hotels/resorts that are typically out of my budget on points and miles. I still treat credit cards like debit cards by paying off the full balance every month. My first serious points/miles card was Chase Sapphire Preferred when they offered me 40k points.

That’s an excellent strategy, Steve. Thank you for sharing that. Glad it worked out and that you’re able to travel now. You have the right idea about treating your credit cards like debit cards and never paying a dime of interest – congrats to you!

Thanks again for reading and commenting!

Wow Harlan! Thanks for sharing a very inspiring story. It’s all too easy to feel overwhelmed and hopeless, and just give up. But you can (almost always) turn things around – and you’re one of the few who took those difficult first steps and actually made it happen. Be very proud!!

Thank you so much, Audrey. The first step is the hardest for sure. After you get a plan, all you have to do is follow the steps until you get back on the right path.

Thanks again for reading all this time.

This is such a nice article. When we’re young, it’s sometimes hard to understand what we’re supposed to be doing. I can feel that pit that you talk about. I know exactly how it feels to wait while the phone rings to talk to someone you’re sure is going to tell you that you are an irresponsible idiot. I just did it…I had to go to the hospital for a kidney infection, and even though I have very good insurance (that I pay for myself, not through work) I still ended up with a couple different $900 bills. I was mad I had to pay them even though I pay so much for insurance. I stomped my feet and cut my nose of to spite my face lol. Luckily I got over my bullshit and dealt with it before they were reported, but goes to show that even these days it happens.

God, dealing with financial stuff still stresses me out. I’m a maniac about paying everything super early and staying caught up but it’s just a fine balance. One little thing can throw it all off and then you’re scrambling and playing catch-up all over again.

The biggest lesson I learned is to communicate, take ownership, and work it out sooner rather than later. If they see you’re trying, you’ll be so much better off than if you let it go. It’s much easier to get it sorted early than clean everything up after the fact.

Thanks for sharing your experience – always great to hear from you, Garrett!

I love this so much and can relate–especially the student loans. It’s my LEAST favorite bill to pay each month. And let’s not get started on medical school loans… But when you make them work, like you did (IBR), it’s not so awful. I’m so glad you hopped into the credit card game. I enjoy your adventures.

Thank you so much, Caroline. Same to you, too. Thank you for sharing your voice and thoughts with the world. I’m always a fan of your wonderful posts. Means a lot. Thank you.

Awww, thanks Harlan. That means a lot too.

This is awesome, and you give me so much hope! I always read about points, travel hacking, and the like, but I just wondered if it would work for someone like me who doesn’t want to really get into debt or spend a bunch JUST to earn points. Thank you so much for this, I think I’m going to take the dive now!

I promise you the end justifies the means – and the end is really cheap travel! I can’t wait to hear about your adventures with this. Let me know if I can help or advise in any way, I would love to be there for you!

wow another one of my favorite bloggers in dfw!!! by chance do you know the hustlermoneyblog team? they’re located in dallas too!

i really enjoyed this post Harlan. I can relate similarly. It’s bloggers like you that got me into this. Cheers!!! Hope to meet you soon.

Also, aside from the bloggers you’ve listed, what are some of your favorite blogs? I would like to see their stories as well! Thank you!

Thank you so much, Scott! I would love to meet you, too – I’ll add a new meetup very soon!

I was going to type out a long reply but I made a new post for you instead: https://outandout.boardingarea.com/bloggers-to-read/

Those are def my fave bloggers. Thank you so much for reading and for your kind words. I really appreciate it! 🙂 And thanks for the heads up about HMB – I did not know that and love them!

Thanks again and cheers!