Happy New Year! I can’t believe it’s 2019! I’m working on travel plans and my credit card strategy – and soon I’ll have gigantic news to share.

If you spent too much over the holiday season, and carrying a balance is inevitable, consider transferring your balance to a new card with a 0% APR period. They vary from 12 months to a staggering 21 months! This will hugely minimize the interest you’ll pay.

Depending which card you get, you won’t have to pay it off until January 2020 at the shorter end – or October 2020 at the longer end. That’s awesome!

Or if you have a big purchase coming up, opening a card with a 0% APR period gives you time to pay it back.

I’ve used both strategies successfully. But beware – pay close attention to the dates (which are listed on every statement you’ll get), or you’ll be right back where you started.

Still, it’s a LOT better than carrying a balance and paying huge interest rates. NEVER carry a balance if you can help it!

Paying interest negates any rewards you earn. Your balance will grow and you’ll get stuck on a debt treadmill – don’t do it!

Here are card options for balance transfers and big-ticket purchases. Because yes, life happens. Just try to control the damage as best you can.

Get unstuck with balance transfer cards

- Key Link: Balance transfer card offers

If you know you won’t be able to pay a credit card balance in full, consider transferring the balance to another card. You’ll pay a fee – usually a percentage of the balance – but it’s worth it to pay say, a 3% fee one time instead of 18+% interest over several months, which is what you’ll find on most premium rewards cards.

Again, if you think you’re in danger of carrying a balance.

You can see cards with current balance transfer periods and fees laid out in simple tables at this link.

Earn rewards with these cards after you pay them down! Get award travel, cashback, and much more. But be aware, you will NOT earn rewards on the balance you transfer

Cards with balance transfer opportunities don’t mean giving up bonus categories, welcome offers, and rich rewards. I was surprised some of the best cards on the market had balance transfer options.

I personally have 3 of these 6 cards. Keep in mind you won’t earn rewards when you transfer a balance. But when you get done paying if off, you’re left with a card that earns points, miles, or cashback – so pick one you want to keep long-term!

Even better, NONE of these cards have an annual fee. So the only fee you’ll pay is to transfer your balance. Beyond that, you can keep them forever as a free way to help age your credit report and boost your credit score.

The 0% APR expiration date is clearly listed on every monthly statement

Just be sure to pay it off before the 0% APR rate expires. You’ll find the date near the bottom of your monthly statement.

If you’re paying high APRs, it could easily be worth it to get 0% APR to give yourself some wiggle room. The one-time fee will be much less than paying interest for months on end.

Citi cards take the cake with up to 21 months of no interest

The Citi Double Cash card has 18 months with 0% APR for balance transfers. The fee is 3% of each balance transferred in, with a $5 minimum.

This card earns 1% cashback on purchases when you make them, and another 1% cashback when you pay it off for a total of 2% cashback (hence the card’s name).

21 months with 0% APR is insane!

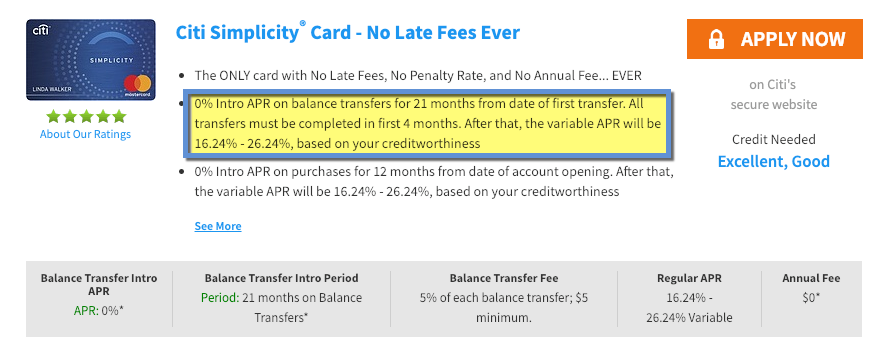

And the Citi Simplicity card has a 21-month 0% APR period on balance transfers when you complete your transfer in the first 4 months of account opening. The fee is 5% of each balance transferred in, with a $5 minimum.

You’ll also get 12 months with 0% APR on new purchases.

Both cards have NO annual fees. Depending on how long you want to carry a balance and how big it is, either card would go far to get you caught up. I’ve personally had the latter and use it sometimes for Citi Easy Deals.

Or make a big purchase and pay no interest for 12 to 18 months

- Key Link: 0% APR card offers

As a homeowner with an aging HVAC system, I rue the day it finally craps out and I have to replace it to the tune of $4,000 to $6,000. You bet when it becomes point critical, I will open a card with a lengthy 0% APR for new purchases to give myself some time to pay it back.

Cards with 0% APR offers can add padding to your cashflow at times you need it most. I used an offer to make a big student loan payment so I could get ahead of the accruing interest on the loan. I ended up saving $1,000s in money that would have gone to interest – without ever touching my principal (which is a thought that kills my psyche, but whatever).

Other big purchases include:

- Vehicle down payments

- Tuition payments

- Home repairs

- Auto repairs

- Medical bills

- Pet surgery

- Any other big expense

Again, the big caveat is to pay off your balance before the intro rate expires. The cards in the table above also have the same 0% APR for new purchases.

Bottom line

- Key Link: Balance transfer card offers

- Key Link: 0% APR card offers

Now’s the time of year where it’s easy to come perilously close to carrying a balance. If you want to collect points & miles, you should never carry a balance because paying interest negates (many times over) any rewards you earn.

But if you have to carry a balance – or just want to with a big-ticket item to ease your cash flow – I recommend opening a new card with a 0% APR offer on either balance transfers or new purchases (or both!).

My gramma had to buy a new stove without much warning right before Christmas

While you won’t earn rewards on balances you transfer, you’ll have an excellent reward card once it’s paid (depending which card you choose). And that’s the kicker – pay it off before the intro rate expires. Many of the best cards with 0% APR also have NO annual fees. So all you’ll pay is the initial balance transfer fee. And then you can keep the card forever to help boost your credit score.

But it can be a slippery slope, so pay close attention and get it paid off ASAP. That said, this route is far easier to get ahead of than getting on a debt treadmill. Used sparingly and smartly, it can give you wiggle room – and time.

Have you used a 0% APR intro rate to avoid interest or make a big purchase?

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!Earn easy shopping rewards with Capital One Shopping—just log in and click a link.

Announcing Points Hub—Points, miles, and travel rewards community. Join for just $9/month or $99/year.

BEST Current Credit Card Deals

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Leave a Reply