Also see:

- It’s Back! 75,000 Hilton Points for Citi Hilton Visa With No Annual Fee

- My Top 5 Hilton Category 2 Hotels for Award Stays

It’s no secret I’m a Hilton fanboy. I lurve them because they make earning points a breeze. And they actually give you a healthy amount of points for staying at their hotels, unlike Hyatt and Starwood (!).

Are Hilton points inflated? Hell yeah. But so are the earning rates.

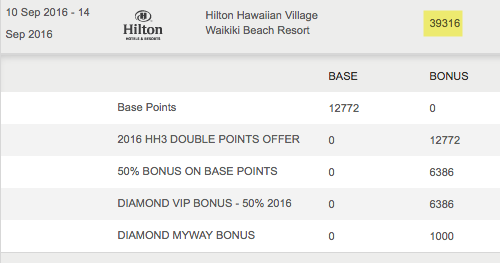

I loved using my Hilton points at the Hilton Hawaiian Village in Honolulu last month

I’ve found good deals with Hilton points, and not because I looked a long time. They’re out there – as with any type of hotel points.

I love the 5th night free perk on award stays when you have any type of status.

And 75,000 Hilton points can be worth over $1,000, as we’ve seen before.

At a bare minimum, there’s no reason why you can’t get $400+ of value from 75,000 Hilton points. Considering the card has no annual fee (and is therefore free to keep), that’s a great deal – and a decent sign-up bonus.

The short

A handy little card with a decent sign-up bonus, if you have a Hilton stay in mind.

The long

- Link: Apply for Card Offers

- Link: Honest Reviews

With this card, you’ll get

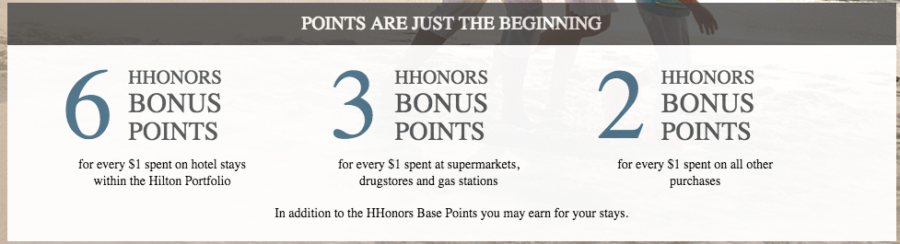

- 6X Hilton points on stays with Hilton

- 3X Hilton points at grocery stores, drugstores, and gas stations

- 2X Hilton points everywhere else

- Automatic Hilton Silver elite status (meaningless, but gets you the 5th night free on award stays)

Decent earning rate

Watch out, though

So here’s the scoop.

Womp womp

Citi is now only handing out bonuses per “family” of cards. That means if you get this Hilton card, you can’t earn the sign-up bonus on the other Citi Hilton card.

Which is the Citi Hilton Reserve – that comes with 2 free weekend nights at most Hilton hotels (even the super luxurious ones), and Hilton Gold elite status. There’s a $75 annual fee on that card, but it can be worth it for the Gold status alone (free breakfast and a decent shot for upgrades). And if you opened OR closed the Citi Hilton Reserve in the past 24 months, you can’t get this new offer.

Arguably, the 2 free weekend nights can be worth… easily over $1,000 if you stay at a hotel where rooms are $500+ a night (they’re out there).

Which one is better for you?

So the road forks in the woods. Which one will you choose? The 75,000 points and no annual fee OR the 2 free weekend nights, Gold status, and $75 annual fee?

Dun dun dunnnnn!

If you like Hilton, the Citi Hilton Reserve is better.

If you already have Hilton elite status and a lot of Hilton points (the boat I’m in), well heck, wouldn’t you like to have 75,000 more points than you already have?

There’s also the issue of how you plan to redeem. Are you thinking special trip (honeymoon, romance, etc.)?

Or do you want some points on hand to fill in gaps here and there? Consider the 5th night free can really boost the value here. That will help guide your decision, too.

A shower of Hilton points

Me, I have enough Hilton points for 2 weekend nights at a super nice Hilton. Would it pain me to redeem 200,000 Hilton points all at once for only 2 award nights? Not really, actually.

Hilton throws points at me left and right by staying regularly and signing up for their promos. Every time I turn around, I have another 100K Hilton points.

To my mind, I’d rather have the 75,000 points free and clear and keep the card forever. Your situation may be different, so give it a think-through before you dive in.

That said, it’s worth it because it’s one of the few cards that earns bonus points at drugstores. If you spend a lot at CVS, Rite Aid, or Walgreens… this card is your friend.

Grade: B

Yeah, it’s “Bitchin’.” Free Hilton points, free to keep, Silver status to get you started, it’ll age your credit, and get you in nicely with Citi.

I wouldn’t touch this card at its usual 40,000 point offer, but at 75,000 Hilton points, it’s worth a look. And, there’s no reason why you can’t squeeze $400 to $1,000+ out of value with this card.

I also wouldn’t apply for this card over others in Citi’s portfolio, but like I said, if you’re looking to score some relatively easy Hilton points, I’d throw it on the pile.

Keep or DTMFA: Keep.

- Link: Apply for Card Offers

Keep it forever. You never know when you’ll want the 5th night free on award stays. Citi is good about applying promotional offers to the card. And retention offers. And it could improve your credit score if you keep it long-term. It’s free to keep and have, so there’s never a reason to cancel.

Also, if this is your only Hilton card, obviously use it for your Hilton stays.

- Capital One Venture X Rewards—Earn 90,000 Venture miles once you spend $4,000 on purchases within the first 3 months from account opening, plus a $300 annual statement credit for travel booked through Capital One

- Ink Business Preferred® Credit Card—Earn 100,000 Chase Ultimate Rewards points after you spend $15,000 on purchases in the first 3 months and 3X bonus points per $1 on the first $150,000 spent on travel and select business categories each account anniversary year

- Amex Blue Business Plus—Earn 15,00 Membership Rewards points once you spend after you spend $3,000 in purchases in the first 3 months of Card Membership and 2X bonus points on up to $50,000 in spending per year with NO annual fee

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

the real question is, how churnable is it even after they implement the change ?

The rule applies when you open OR close the card.

So if you want to earn the bonus again, you’d be better off closing the card rather than keeping it open. Just keep track of when you close it so you can reset the timer.

That’s the only way around it I can see.

I tried getting it last week. Citi denied me. They must only accept deadbeats whom they think they can make fee income off of.

Meanwhile, applied to the Hilton AMEX ~230 am that same night. (Right before Citi, as AMEX has the superior offer/terms.) 1044 am the day (32 hours!) after UPS delivered that Hilton AMEX. It’s genius promotional budget: I’ll tell everyone for weeks to come how quickly AMEX delivered my card when there clearly was no rush and, as such, theirs will clearly be my card of choice.

Meanwhile, it’ll take several times as long to see Citi’s reason for rejection in the mail.. not that I’d expect much from such corporate welfare trash.

I have both cards. It actually took AMEX two weeks to approve my application that went straight to pending. But Citi approved me instantly and sent the card right out. Who the heck knows any more lol

Still deciding whether to call their recon line when (or before) the reason for denying me arrives in the mail. Obviously not a huge (or even small!) hotel user, but seems a fun game to begin banking awards heading into the holiday season.

As for card 2x points on drugstore purchases, even my ancient Amazon visa (via Chase) could turn that trick. When I analyzed whether to get the Hilton AMEX (bonus offer tipped the scale), kind of thought of it as an alternative to the Blue Cash Everyday card.. though got that one back in 2014 when they had the $250 cash (automatic statement credit!) on 1000+ 90 day spend. 🙂

As for the annual fee Hilton AMEX, again they’d crush citi if AMEX just eliminated the foreign exchange fee.. as kind of weird for an annual fee card with what is now the world’s second biggest hotel chain.

my dear friend you bought a baubax jacket small size pleast tell me your height & weight i also want to buy one,thanks

I was denied for that card for the 2nd time and approved for the Citi Prestige. Go figure Citi!!

Hi Harlan, I haven’t commented on your posts lately but always check in. Didn’t you have the Barclay Arrival + in the past? If so, here’s a request for your review of that with the current 50K offering.

Great to hear from you, Dustin! Here’s the review: http://outandout.boardingarea.com/honest-review-barclaycard-arrival-plus-50000-mile-offer/

Hope you are well – and thank you for checking in!

Oh thanks! Not sure how I missed it:) Doing well and looking forward to the next trip. Take care!