The credit card landscape is shifting fast:

- Chase will apply the 5/24 to all its cards starting in April 2016, including co-branded and business cards

- Citi has been shutting peeps down for usage they don’t like (multiples of any 1 card, money order payments, etc.)

- Barclays had a good product with the Arrival Plus card, then butchered it. That was pretty much the only good card they had

- US Bank is useless

- Bank of America is only good for the Alaska Visa

- Wells Fargo is a cantankerous little beast

- There are a few other niche cards, like the Fidelity Visa and BBVA NBA card, worth looking into, but not many

Card offers come and go. Benefits change. Mergers happen and shake things up. Revenue-based elite status throws a wrench into points-earning calculations.

Could ThankYou become the go-to?

Lately, I’ve been using my Citi cards for most of big purchases. And my trusty Chase Sapphire Preferred for dining.

Non-bonused spend goes on the Fidelity AMEX (I still have the AMEX version). And that’s pretty much it. All the other cards I have are for niche benefits or very specific spending (Chase Hyatt Visa, for example).

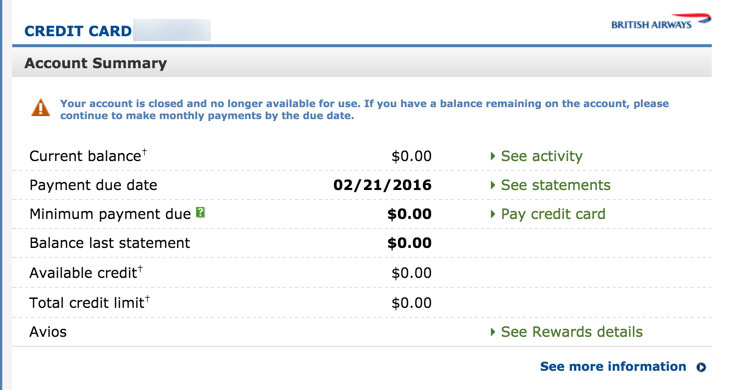

Recently, I went ahead and canceled the Chase British Airways Visa.

Bye, you useless thing

And downgraded my US Bank Club Carlson Visa Signature to the no annual fee version just to keep the credit line and history intact (here’s my recent offer to increase my credit line in exchange for 250 Club Carlson Gold points).

Poor AMEX

AMEX in particular keeps taking the hits left and right:

- Costco gone to Citi

- JetBlue gone to Barclays

- SPG merger with Marriott gone to Chase

But they’ve thrown a few punches, too. Terrible sign-up bonuses and restricting all cards to 1 sign-up bonus per LIFETIME.

Dead to me

You could reward customers with a bonus every few years, at least. Once per lifetime seems unnecessarily harsh.

I explored the topic of switching away from AMEX and over to Citi a few months ago.

As I shift more spend to Citi (and specifically to my new Citi AT&T Access More card – which is also the best card for shopping at Costco), I’m now thinking of canceling other cards to earn ThankYou points. Because I haven’t been hitting 30 transactions per month on my AMEX EveryDay Preferred card, which means no 50% bonus.

And let’s be honest, Membership Rewards is kind of a mess.

What’s coming and going

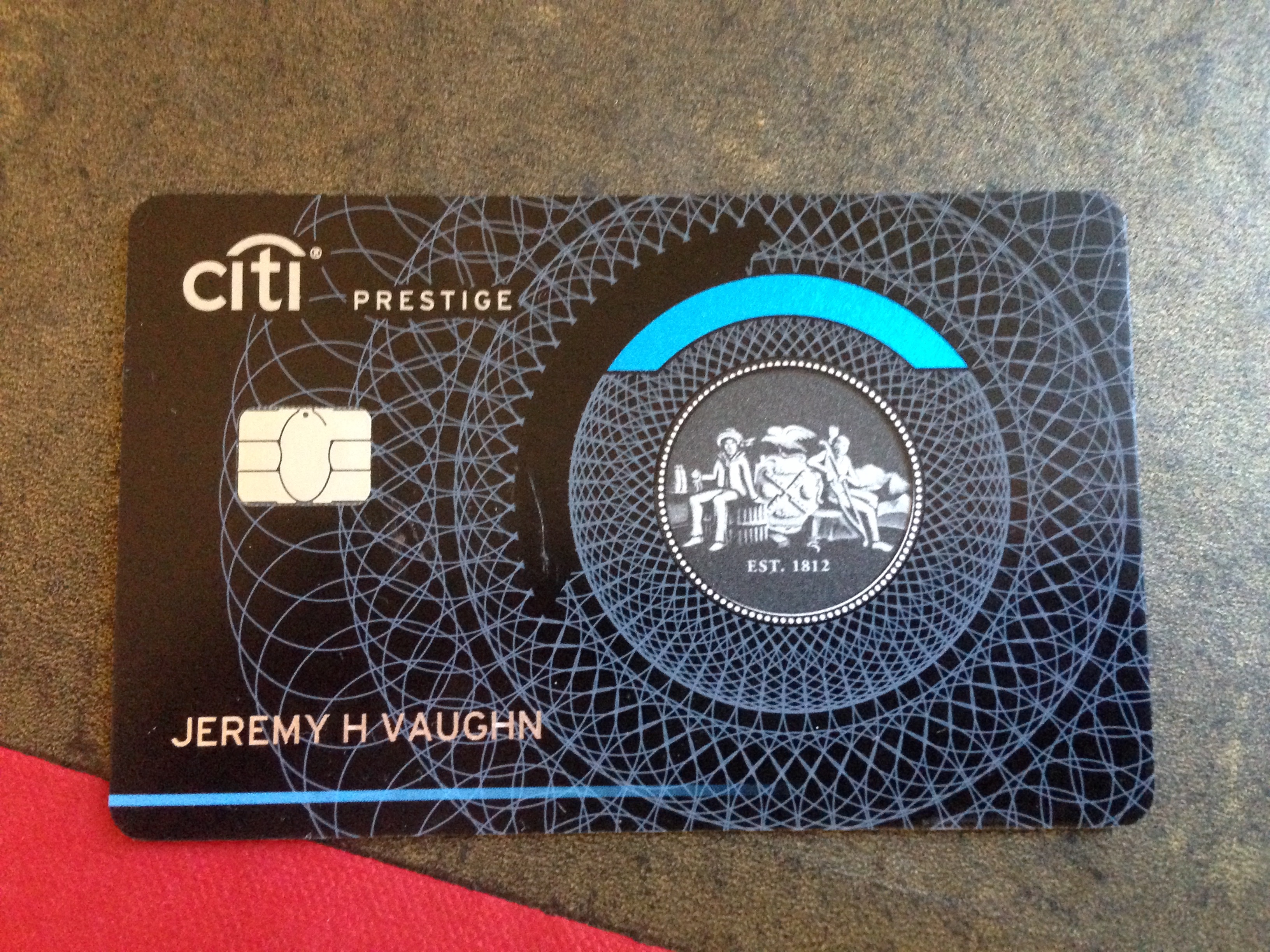

I’m loving my Citi cards more than ever. Citi Prestige is the gift that keeps on giving and Citi AT&T Access More is amazing for online shopping. I still use my Chase Sapphire Preferred for travel other than airfare and hotels, and for dining.

Picture of bae

Until Citi adds a meaningful domestic airline partner, ThankYou won’t be my program of choice. I still use Ultimate Rewards for British Airways, United Airlines, and Hyatt transfers the most.

I might get one more Chase card before the 5/24 rule goes into effect, with the understanding it will likely be my last. 🙁

And other cards have to go, including:

- AMEX EveryDay Preferred (not worth the $95 annual fee if I’m not triggering 50% bonus)

- Barclaycard Arrival Plus (no better than a 2% cash back card now. $89 annual fee not worth it)

- Chase British Airways (already canceled. When they cut 1.25 points on purchases, it became useless)

- US Bank Club Carlson Visa (no more BOGO and $75 annual fee – downgraded)

I’d like to add the Citi ThankYou Premier to my staple at some point. And maybe another AAdvantage card just for the miles. Wouldn’t mind the extra Hilton points with the AMEX Hilton Surpass, either.

Or the Chase British Airways card for another 100K Avios. This will likely be the last Chase card I get. :/

But that still leaves Citi cards getting the bulk of my actual ongoing spending. Which is kind of surprises me.

My favorite way to redeem Citi ThankYou points is for flights on American Airlines through my Citi Prestige card.

And I need to look into Singapore Airlines’ KrisFlyer a little more… because there are good values for domestic award flights, and flights to the Caribbean. Citi ThankYou points are also crazy easy for me to earn. So it might be worth paying a little more for award flights because of how easy it is to accumulate them.

Bottom line

Citi cards have become the dark horse in my wallet lately. And increasingly, I’m finding it’s more worthwhile to cancel other cards, like the AMEX EveryDay Preferred, or downgrade them, like the US Bank Club Carlson Visa, and keep Citi cards in rotation.

The Citi AT&T Access More card has unexpectedly become my jam.

And I’m loving getting free flights on American Airlines to earn Alaska Airlines elite status with Citi Prestige.

I’m also finding lately I want more Citi cards than Chase or AMEX or any other bank… which is also something new.

Have any Citi cards moved up in your wallet? Are there any others you’re looking to downgrade or cancel?

And… any thoughts on Citi’s ThankYou program? What would you like to see change or added?

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!- Capital One Venture X Rewards—Earn 90,000 Venture miles once you spend $4,000 on purchases within the first 3 months from account opening, plus a $300 annual statement credit for travel booked through Capital One

- Ink Business Preferred® Credit Card—Earn 100,000 Chase Ultimate Rewards points after you spend $15,000 on purchases in the first 3 months and 3X bonus points per $1 on the first $150,000 spent on travel and select business categories each account anniversary year

- Amex Blue Business Plus—Earn 15,00 Membership Rewards points once you spend after you spend $3,000 in purchases in the first 3 months of Card Membership and 2X bonus points on up to $50,000 in spending per year with NO annual fee

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Excluding cash back cards, I’d add that the B of A business Alaska card is worth grabbing from time to time as well — I frequently sign up for the personal and business simultaneously, net $50 out of pocket in fees for 50k miles. And one could argue that the Lufthansa card (when it jumps up to 50k) is another solid Barclays option, decent program for redemptions in the Americas. I’ve only gotten it once, which speaks to how much more valuable other options have been, but it jumps up the list as the United, UR, and MR cards / bonuses become unattainable.

You’re right, we’re gonna have to start mining the heck out of other cards (such as the Barclays Lufthansa card). Agreed re: BofA Alaska cards. It’s becoming by program of choice, so I’ll need to cozy up to Bank of America. Amazing how things have progressed over the past year.

I’m doing exactly what you are doing. Weening off of all other cards accept for my CSP and putting all my spend on Citi cards in order to get TY points for AA flights and crediting them to Alaska.

I agree that it would be nice if Citi added a domestic transfer partner for TY points but I feel that would draw too much attention to the program and then a devaluation could follow in the future. There is already some okay partners with good uses in them. And even though we can’t transfer to AA we can still transfer to Etihad and use their miles on AA flights.

I’m loving the cards as well and all the changes AMEX and Chase have been doing recently have just pushed me more to cement the switch.

TYP doesn’t need a “meaningful domestic partner” so long as it has SQ. KrisFlyer is better than MP for flying domestic UA J, as they only charge 20k (30k for Hawaii).

Otherwise I totally agree, I got my wife the Thank You Premier before it dropped from 50k and just tell her to use it for everything. Its category bonuses are so comprehensive it really simplifies things for non-experts.

Excellent counterpoint and observation!

I’m still organizing my thoughts about it. I really like British Airways and Hyatt, and transfer to them often.

But you’re right about the Citi TYP. Great card to start with, especially if you want to keep it super simple!

Man your post is too simplistic. There are a lot of good cards both to keep and to churn the sign up bonuses (sometime variable) from all the banks you mentioned.

It’s getting harder with Chase and AMEX already severely restricted any type of card churning. I’d love to hear your favorite cards from the other banks mentioned. Always open to re-thinking a strategy!

I’m just listing some cards that worth looking into either for the bonus or just regular spend.

USBank: korean (30k now), club carlson, cash+, all flex perks cards.

BofA: BBR, Virgin (when they increase the bonus), TR

Barclays: Wyndham, Jetblue (to be fair, it’s offered after your post), Hawaiian, Lufthansa (50k now), Sallie Mae (if it comes back), Upromise is also interesting

TD: Aeroplan

Discover: Miles

CNB: That card!

Marukai: That card!

and so on.

I wasn’t sure whether you are talking about ongoing benefits or bonus and just named a bunch of interesting cards that either have a decent bonus or good for spending.

How can you get miles on Alaska for an AA award flight?

When you redeem Citi ThankYou points for AA flights, it’s treated as a regular revenue flight, NOT an award flight. So you can credit it to Alaska Airlines, or any of their other partners, and earn miles for the flight: https://www.alaskaair.com/content/mileage-plan/partners/american.aspx