I opened 3 new checking accounts last week. And will earn a total bonus of $900 after making the required number of transactions and/or direct deposits.

That’s a super easy way to make $900. And I didn’t even have a credit pull.

Boom

I have around 30 credit cards. And currently can’t get most Chase, Citi, or Amex cards because:

- Chase has 5/24

- Citi limits to “family of brands” every 24 months when you open OR close an account

- Amex has the once per lifetime (AKA every ~7 years) rule

I’m not interested in any Barclaycards. Or US Bank cards. And I can’t get more Discover cards (limit 2).

I’m really only dealing with Bank of America these days for Alaska miles from credit card sign-up bonuses. Except for when there’s an odd offer here or there.

So, scraping the bottom of the barrel. But it’s not so bad down here! I’ve been following more checking account bonuses recently – a new world indeed.

How I got $900 in a week from checking account bonuses

First of all, Doctor of Credit is the source for checking account bonuses – I follow them on feedly.

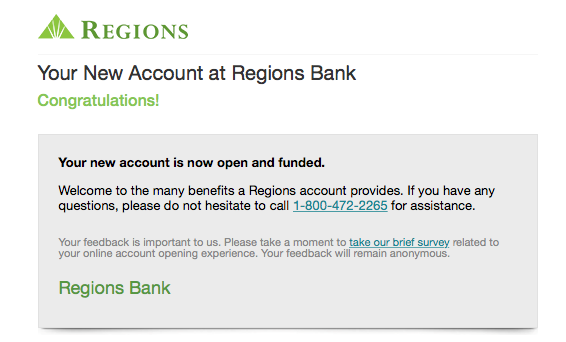

The first bonus was $450 from a new Regions account. My mom banks with Regions, so I had her refer me to a new account. She’ll get $50 and I’ll get $400 – $450 in total.

I opened the account online. And then had to go in person to “sign the signature card” (???). It seemed like a waste of time. But I wanted to ask about their business checking and mortgage opportunities just in case. Plus, it’s always good to have a relationship with a new banker.

The signature card thing took all of 2 minutes. Then we chatted about investment properties and getting a DBA on file – super helpful stuff.

That got him talking about another $200 for opening a new business checking account.

Yessss

He said I could refer myself to that account from my newly opened personal checking account and earn $50 for the referral. And $150 for opening it.

I went back a few days later and opened the account.

So we’re up to $650 for the 2 accounts. I was already beyond thrilled. And I legit needed to open a business checking account with a DBA on file.

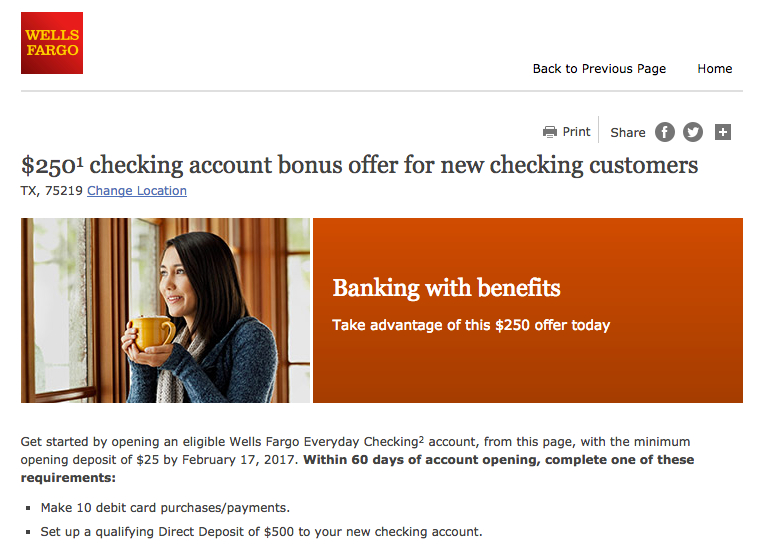

Then, I saw I could get an easy $250 by opening a Wells Fargo checking account.

Bait taken

I could theoretically transfer $500 from Regions to Wells Fargo (then make 10 debit card transactions) to satisfy the requirements. Within a few minutes, I filled out the application and sent it on its way.

So when that cash hits, I’ll be up to $900 earned from checking account bonuses. That’s pretty cool.

What to look out for

It’s not all sunshine and fields of cash.

Then again, neither are credit card bonuses. With those, you have to spend $X,000 amount and track it for X months.

With checking account bonuses, you have to make XX transactions and/or direct deposit $X00 within X months.

There are ways to earn both types of bonus within a few minutes. I’m not worried about it, but it’s a consideration.

I just make sure I track when I met the requirements and when the bonus is supposed to hit in case I have to follow up.

The bigger issue is the recurring monthly account fees, usually around $10. There are ways to waive them, but you have to be on top of it – for at least for a few minutes per month. Then, once the bonus cash hits, you can simply close the account. Or if you like it for other reasons, keep it.

Usually, the fee is waived for a month or two anyway. And I recommend paying it for a couple of months anyway (or getting it waived) just so it doesn’t look as obvious that you only wanted the bonus.

It does require some tracking, time management, and mental headspace keeping track of it all. But again, so do credit card bonuses…

Bottom line

Checking account bonuses aren’t as sexy as 100,000 point sign-up bonuses and award trips in international First Class. But $900 relatively free and clear – who wouldn’t want that?

Because I can’t get most current credit card offers, I’m paying attention to checking account bonuses more (and a huge thanks to Doctor of Credit for tirelessly tracking them all). It’s a whole new world with new rules and guidelines.

But the way I see it, a few minutes of time this past week nearly paid my mortgage for a month.

I know other peeps must be in a similar position. Would you consider signing up for checking accounts while you wait for the next eligible credit card deal?

* If you liked this post, consider signing up to receive free blog posts in an RSS reader and you’ll never miss an update!- Capital One Venture X Rewards—Earn 90,000 Venture miles once you spend $4,000 on purchases within the first 3 months from account opening, plus a $300 annual statement credit for travel booked through Capital One

- Ink Business Preferred® Credit Card—Earn 100,000 Chase Ultimate Rewards points after you spend $15,000 on purchases in the first 3 months and 3X bonus points per $1 on the first $150,000 spent on travel and select business categories each account anniversary year

- Amex Blue Business Plus—Earn 15,00 Membership Rewards points once you spend after you spend $3,000 in purchases in the first 3 months of Card Membership and 2X bonus points on up to $50,000 in spending per year with NO annual fee

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Test test testing!

I posted earlier today and never saw it here. In case you’re testing to see if there is/was a problem.

Oh man, that hurts my soul to think of how many reader interactions I’ve missed.

There was a glitch and I can’t really pinpoint exactly when it happened. It’s been fixed, though. I basically had to unplug everything and connect it again. So all the stats on my side show up as being brand new. I’ll miss having the history, but staying connected is way more important.

Do you happen to remember your question/comment from earlier? I’d still love to hear about it!

Thank you!

The most recent was about ChexSystems and its effect on the checking account bonus. 80% of banks uses the service. It has reports and scores (100 to 899) based on banking (non-credit) accounts. It has stats such as number of inquiries, new application (checking mainly) in the last 90 days, check orders over the last three years, etc.

To many accounts applied for can set off red flags.

So, bottom line, it’s kind of like a credit report for checking accounts, and in a way too many pull can still potentially hurt.

I think I sent a comment on 1/21 Hilton Reserve card also. How long do you think comments have been down (ie. how long ago was the last comment other than your own)?

Ah, crap! What was the one about the Hilton Reserve (if you can remember)?

(And thanks for the detailed information re: ChexSystems!)

It’s hard to tell when the last real comment was. Because there were 2 versions of the site – the “real” version and a “staging” version that WordPress uses (mostly when you migrate themes). Somehow, my entire site was on the “staging” version and some comments still made it through. But I guess others didn’t. So I can see comments from both versions of the site and have no way of knowing what didn’t make it through.

BoardingArea is trying to combine both sets of comments onto the “real” version of the site right now but no doubt some of them fell through the cracks. I’ve been getting comments consistently – but only from the staging version and not the real version. The last comment I can see on the real version is from early January 2017 – so about a month. I don’t know at what point the site got switched to the staging version, though.

I hope that makes sense. It’s super confusing and I feel terrible that I’ve missed so much. But glad it’s worked out and happy to hear your tips and insights – thanks for sticking through this!

There are two major systems – ChexSystems, and also Early Warning Systems (EWS). There can be different criteria for opening an account – some banks will accept customers via a local branch but will reject them if they apply online, presumably because if you apply in person they know that your appearance matches the driver’s license and that could lessen the risk of the new account. (e.g. Santander)

Financial institutions are also starting to turn to social media sites to verify information about their account customers. There may also be a soft or hard pull on other traditional credit reports. In some cases, this might lead to another offer, such as a pre-approved credit card offer (e.g. Huntington, Citizens Bank)

On the Reserve offer it was that it’s not a new offer. I’ve been seeing it for a year. I never saw it as being worth it with no bonus. I did get the Reserve with two weekend nights after spend (don’t recall amount) last year. Of course that was a new card – not an upgrade.

That must have been a bad feeling doing posts and thinking you were getting no comments at all.

Oh wow. It was the first time I’d ever seen it (or I guess been targeted for it). Thanks for sharing that.

And yup, I thought it was because I smelled bad. Well, I still smell bad but at least now I know that’s not it. 😉

Nah but for real, I did see a few slip through. Now that I realized what was happening, I just hope no one thought I was ignoring them or anything like that. 🙁

But all seems fine now – hopefully it’s fixed once and for all! Although I suppose glitches are a part of running a blog, here and there. I’ll do my best to make sure it doesn’t happen again.

Ignore “no comments” part. I guess you were seeing some comments – just not all.

It’s all good, I understood what you meant. Thanks again for sticking by throughout!

Why no Barclaycard cards?

I suppose I could get another Arrival Plus. But what else is there? The JetBlue Plus card? Anything else worth getting?

AAdvantage and Hawaiian Airlines cards.

Cheers,

PedroNY

I’ve heard good things here and there about the Lufthansa card. And the Wyndham card can be alright if you have a specific destination in mind.

Thanks for the suggestions – I might pick up that AAdvantage card in the near future.

If you need suggestions for Wyndham All-Inclusive resorts, I have them right here : )

http://first2board.com/giddyforpoints/2017/01/wyndham-inclusive-hotels-points/

^^^ These are exactly the reason why I’d consider a Wyndham card.

I’d wait until the 3-night (45,000 point) offer returns, though.

Thanks for adding that resource!

I do several of these each year, which helps offset some of my travel costs. However, the issue is the new checking account bonuses are taxable, while credit card sign-up bonuses are not. Credit card bonuses are deemed to be a rebate on spend, while checking account bonuses are income.

Now there’s a hatchet thrown into the mix. I definitely didn’t consider that. So basically, go ahead and lop off 30% every time.

Thanks for the guidance – worth keeping in mind for sure.

I do bank bonuses several times a year too. Just don’t forget about those 1099s. I had did a bank bonus to earn Alaska miles and I got a 1099 for it. I forgot to include this in my tax return and got a letter from the IRS that I needed to include it. Just a heads up!

Wow, that’s intense! Good to know – thank you, hugely useful tip!

Just heads up, this post made it into my TBB Buzz post tomorrow. Along with that Hyatt Cancun food feast piece. Nice job!

Oh my gosh! I’m TBB famous. Thank you, George! I still read ALL of your posts -thank you!